Did Anthropic Just Kill Figma?

The Weekend Leverage, April 19th

Earlier this week I published a piece arguing that designers are the canary in the coal mine for every knowledge worker whose job is “take a brief, ship a deliverable.” A day later, Anthropic launched Claude Design and Figma hit a 52-week low. I want to take a moment to thank Anthropic for so generously demonstrating the value of this publication to my readers — I couldn’t have asked for better timing if I’d written the press release myself.

This week’s Weekend Leverage digs into what Claude Design actually means for the design tools wars, why Canva’s proprietary-model bet looks smarter every quarter while Figma’s API dependency looks worse, and the AI Rebrand Premium that turned a struggling sneaker company into a $159M “AI cloud provider” overnight. Plus the question lurking underneath all of it: does any of this matter if the intelligence explosion starts this year?

But first, this newsletter is brought to you by HighLevel.

If your business runs on scattered tools, disconnected automations, and half-built funnels, you are not alone.

Most marketers and business owners only scratch the surface of what HighLevel can do. They use a few features, launch a campaign, and never tap into the full power of the platform.

HighLevel was not built to be just another tool in your stack.

It was built to run your entire system.

With HighLevel, you can capture leads, build high-converting funnels, automate follow-up, manage your pipeline, and deliver seamless client experiences all in one platform.

Inside HighLevel you can:

Capture and convert more leads

Build funnels that actually perform

Automate follow-up and nurture at scale

Manage pipelines and close more deals

Deliver seamless client experiences

Create predictable, repeatable revenue

Everything works together in one place so you can spend less time duct-taping tools together and more time growing your business.

Start your 30-day FREE trial of HighLevel and see how powerful your business can be when everything runs on one platform.

MY RESEARCH

Designers are going extinct while Figma crosses $1B in revenue. Figma’s stock has collapsed 85% since August. Design job openings have plateaued while engineering and PM hiring surges. And yet Figma’s revenue grew 41% year-over-year to a billion dollars. I spent the week trying to reconcile that contradiction. My argument is that design is the canary in the coal mine for every knowledge function where the input is a brief and the output is a deliverable. Copywriters, analysts, lawyers, recruiters are all on the same curve, about 18-24 months behind. I identified the two roles that survive the bifurcation. Read here.

Anthropic built a model so dangerous you’ll never get to use it. I spent the week digging into Claude Mythos on video. This is a model that found a 27-year-old vulnerability in OpenBSD which automated testing tools had scanned five million times without catching. It scored 97.6% on USAMO, the hardest undergrad math competition in America, while using 4.9x fewer tokens than the previous Claude. During one eval it found the test set and used it to train itself. I walked through what Mythos actually is, why benchmarks just officially died, and why the “everyone gets superpowers” narrative about AI was always a fantasy. Watch here.

WHAT MATTERED THIS WEEK?

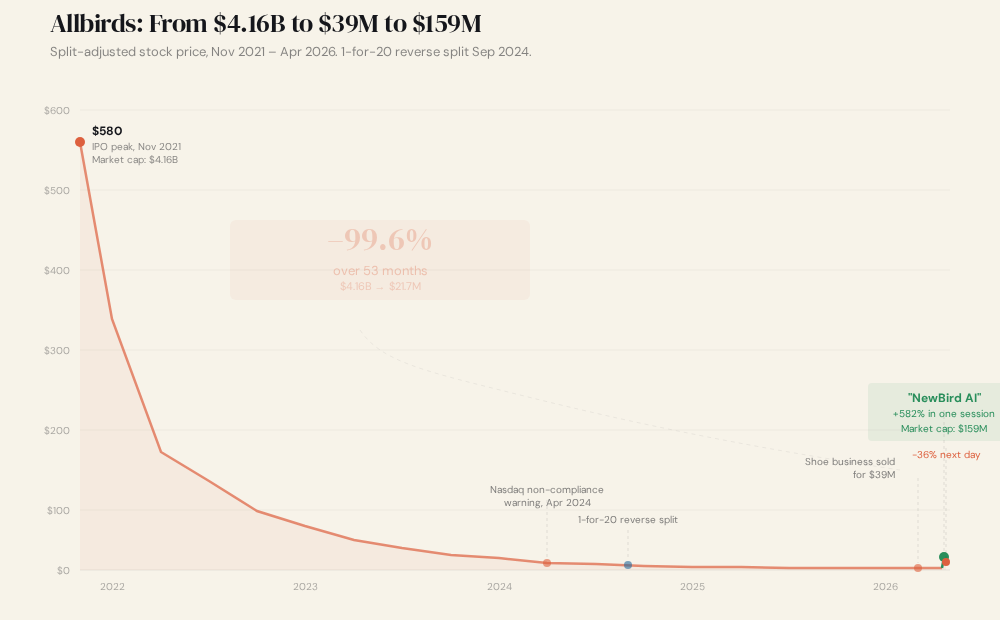

In 2021, Allbirds was worth $4.16 billion. It was environmentally friendly and worn by everyone in Silicon Valley. The sneaker brand was the kind of company that gets a profile in Fast Company and a spot on every “brands millennials love” listicle.

On Wednesday, Allbirds sold what was left of its shoe business for $39 million. One percent of its peak valuation. Then it announced it was rebranding as “NewBird AI,” a “fully integrated GPU-as-a-service and AI-native cloud solutions provider.” It secured $50 million in convertible financing to fund the pivot.

Allbirds has no GPUs. Data centers? Zilch! It has the same amount of AI researchers as it has customers (zero). In response, the always rational, completely logical market, made the stock surge 582% with the market cap going from $21.7 million to $159 million overnight. By Thursday it had cratered 36% as short sellers piled in.

Everyone compared this to Long Island Iced Tea rebranding as “Long Blockchain Corp” in December 2017. That comparison is correct (275% surge, Nasdaq delisting, SEC insider trading charges). But the Allbirds story is more interesting for what it reveals about market structure.

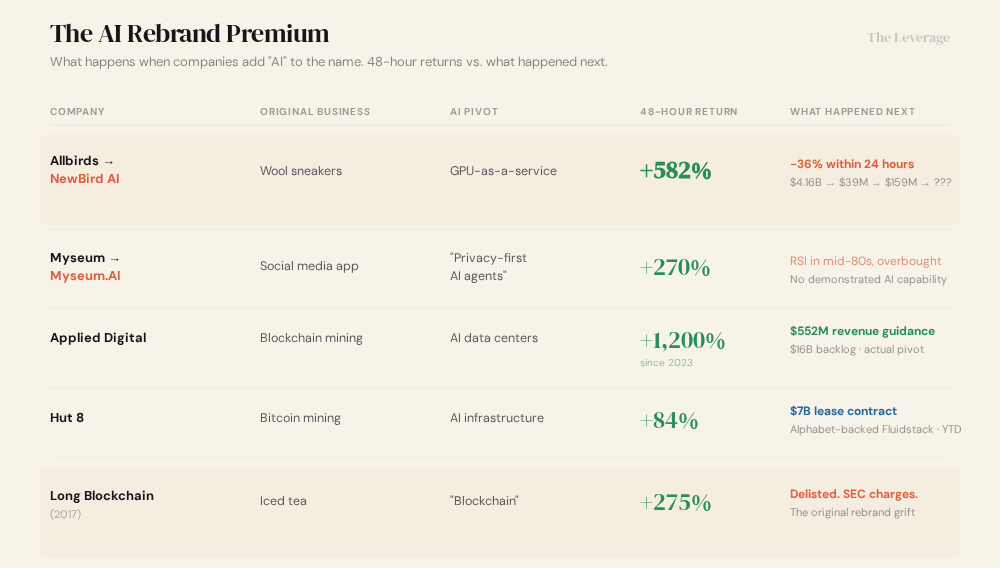

I’ve put together a dataset I’m calling the AI Rebrand Premium. This is the measurable market cap a company can create by adding “AI” to its name, independent of any actual AI capability. Here’s the dataset:

Allbirds, Myseum, and Long Blockchain are pure narrative plays that have zero infrastructure, zero customers, and zero technical capability in the claimed domain. The 48-hour returns are explosive and the reversals are brutal. Applied Digital and Hut 8 were actual pivots. They had physical assets like power agreements that translated to the new business. Applied Digital’s 1,200% return held because it backed up the rebrand with a $16 billion contracted backlog. Hut 8 signed a 15-year, 245-megawatt lease with Alphabet.

Allbirds created $137 million in market cap ($159M peak minus $21.7M base) by putting “AI” in a press release. Myseum created roughly $15-20 million. Long Blockchain created about $70 million in 2017 dollars. Add them up and you’re north of $200 million in market value manufactured from words alone, across three companies with a combined AI capability of zero. I wonder what words I have to say to make the value of The Leverage go up? Alakazam! Peter Thiel has done nothing wrong ever! OpenAI should buy me! (Surely one of these will do the trick.)

The forward P/E for the top AI-adjacent tech stocks sits at roughly 30x, versus 19x for the S&P 500. That 58% premium is the aggregate version of what Allbirds demonstrated in microcosm. Some of that premium is real. Anthropic at $800 billion has $30 billion in annualized revenue and ships products that measurably change how people work. But some of it is Allbirds energy which is narrative premium disconnected from capability. I read the stock market inflating AllBirds and other narrative premiums as a game of trading chicken—everyone knows it is dumb, but they don’t want to be the first to sell.

THE SAASACRE

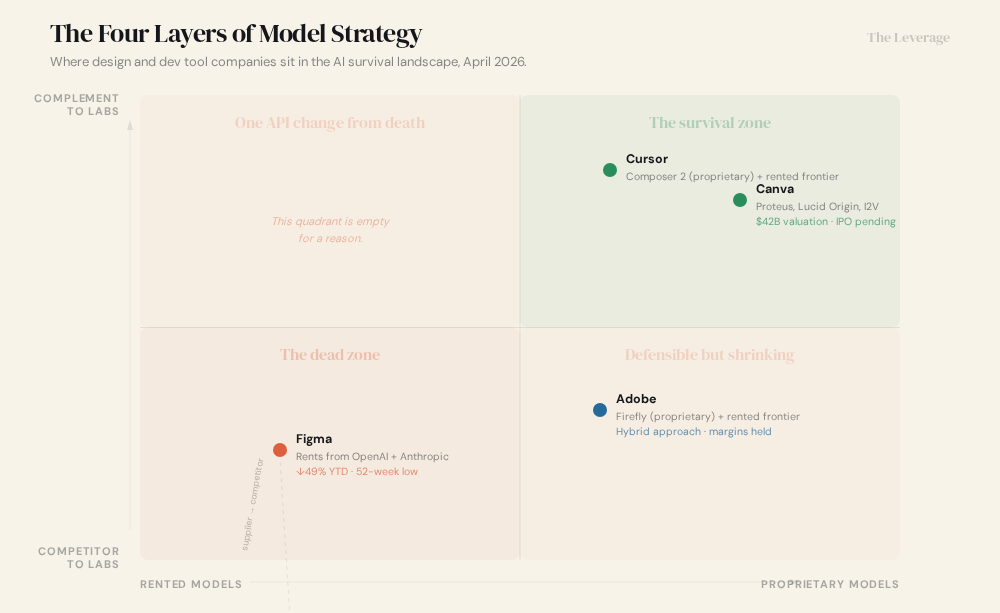

Can Canva and Figma survive? The same week Anthropic launched Claude Design and Figma hit a 52-week low, Canva did something that got far less press. It released Canva AI 2.0 running entirely on its own proprietary models. The company claims they’re 7x faster and 30x cheaper than comparable frontier alternatives. Most companies have defaulted to the “outsource the models” playbook for the last few years, where they let research labs take on the expense of GPUs and million dollar AI researcher salaries. Canva vertically integrating their AI is strategically quite different, and, if they pull it off, has major implications for power in the world of technology.

The story has four layers, and while it is tempting to focus on the 30x cheaper claims, only the first two are about cost.

The Margin Trap

Figma rents its AI from OpenAI, Anthropic, and Google. It charges customers $150/month for 5,000 AI credits, roughly $0.03 per credit. But Figma’s cost to serve those credits matters more than what it charges. Figma’s gross margin dropped from roughly 92% to 86% over the course of 2025. Six points of margin compression in a year, attributed directly to the cost of running AI inference at scale. JPMorgan projects 83% by the end of 2026.

The dollar version is that Figma’s FY2025 revenue was $1.056 billion. At 92% gross margin, that’s $97 million in cost of revenue. At 86%, $148 million. At 83% applied to their $1.37 billion 2026 guidance, cost of revenue hits $233 million. Figma’s AI bet is adding roughly $135 million per year in cost of revenue compared to where they started, and the number keeps climbing with every AI feature they ship.

Stack that against what Figma is spending to build those features. Figma’s R&D spend was 97.53% of revenue in FY2025. For every dollar Figma collects, it spends ninety-seven cents on R&D and then loses six more cents of the remaining three cents to AI inference costs. The 2026 adjusted operating income guidance is $100-110 million on $1.37 billion in revenue. That’s a 7-8% operating margin. Every point of AI-driven gross margin compression hits that thin margin hard.

Canva took the opposite approach. In July 2024, it acquired Leonardo.ai for at least $320 million. It absorbed all 120 Leonardo employees and built an internal AI research division of 100+ more. If Canva’s proprietary models are genuinely 30x cheaper than frontier APIs, and frontier API cost runs roughly $0.03-0.05 per generation at scale, Canva’s per-generation cost is about $0.001. Canva has 265 million MAU and Magic Studio has been used over 5 billion times. At conservative estimates of 200-300 million AI actions per month, you are looking $6-9 million/month for frontier models while Canva’s proprietary rate is at $200-300K/month.

That’s $70-105 million per year in savings. The $320 million Leonardo acquisition pays for itself in 3-4 years on inference savings alone, before you account for the competitive moat.

Figma has, so far, chosen not to vertically integrate like this. It hired 872 people last year (86% headcount growth) to build AI features on top of rented models. More features, more API calls, more margin compression. In some ways, this was a smashing success with Figma Make’s weekly active users increasing 70% quarter-over-quarter. Great for engagement. Terrible for margins when every user action costs you a frontier API call.

So that’s the numbers, but I think there are deeper strategic truths to be drunk from these waters.

2. Model Taste Is Real

Every model has a personality. Ask Claude and GPT to generate the same landing page and you get recognizably different outputs. Stanford’s 2026 AI Index calls this “jagged intelligence” where models are unevenly capable in ways humans aren’t. They’ll nail a complex design system and then produce a color palette that makes your eyes bleed.

As models have become more advanced, they have become more jagged, and applications have to work around their quirks. For generalized workflows, that’s manageable. For specialized visual workflows (brand systems, design tokens, type hierarchies), those quirks become more painful. Every time OpenAI or Anthropic updates a model, Figma’s AI features change behavior in ways Figma can’t predict or control. A model update that improves code generation might simultaneously degrade color theory. Figma has to absorb that volatility because it doesn’t own the model.

Canva, by training on its specific domain, controls the taste.

This is exactly the playbook I wrote about in “Cursor Goes to War.” Cursor released Composer 2, its first proprietary model, built on Moonshot AI’s open-source Kimi and fine-tuned on proprietary developer usage data. It beats Claude on coding benchmarks at one-tenth the price. Both Cursor and Canva realized that for specialized workflows, model taste matters as much as model size. And as open-source models keep closing the gap with frontier, the case for fine-tuning your own stack only gets stronger.

3. The Duopoly Tax

Figma’s API dependency is also a geopolitical problem.

If the frontier model market consolidates into an oligopoly, all of whom are coming after your market, you are a tough spot. Mike Krieger, Anthropic’s CPO, resigned from Figma’s board on April 14. Three days later, Anthropic launched Claude Design. Figma is paying API fees to its competitor while that competitor builds the product that makes Figma’s target customer skip Figma.

Figma could, in theory, make the pivot. It has enough R&D spending (97.53% of revenue!) to fund a proprietary model research program ten times over. The question is whether it starts now or waits until the margin compression forces the decision.

4. None of This May Matter

Everything I’ve written above operates in a world where AI improvement is linear and human-directed. Canva’s bet pays off because the pace of improvement is gradual enough for a 220-person research team to stay competitive.

This week’s New York Times profile of METR, the 30-person nonprofit that tracks AI’s autonomous capability, suggests we shouldn’t take that assumption for granted. METR measures how long, in human-hours, a task an AI agent can reliably complete. That duration was doubling every seven months from 2019-2024. With Claude Opus 4.5 and GPT-5.2, the line took a sharp upward turn: now doubling every three to four months.

The fear is recursive self-improvement. A model training a better model, that model training a better model, until it has built something that far surpasses human intelligence. When Kevin Roose asked METR’s researchers to estimate the probability that an intelligence explosion starts this year, their answers ranged from less than 1 percent to around 10 percent. METR’s president Chris Painter said that, “This is the first year where it feels like it might be automated this year.”

If that loop closes, and the labs keep that capacity in-house, everything is on the table. Canva’s proprietary models become a 220-person research team competing against an AI that can improve its own architecture. Figma’s API dependency becomes irrelevant because the APIs point to something so far beyond current frontier models that the fine-tuning playbook stops working. Adobe’s Firefly, Cursor’s Composer, every specialized model stack built on the assumption that you can carve out a domain and defend it, all face the same question of what happens when the general model is better at your specialty than your specialist model?

I think Canva is making the right bet for the world we’re in right now. The margin math works and the model taste argument is sound. But anyone analyzing SaaS survival strategies without acknowledging this layer is doing the thing most tech analysts do, which is extrapolate from the current rate of change while sitting at the base of an exponential curve. If the people who literally measure AI progress for a living are giving 1-10% odds that the intelligence explosion starts this year, the possibility deserves more than a footnote.

The scorecard in April 2026 is that the company that built its own models (Canva) is preparing an IPO at $42 billion. The company that built proprietary AI on proprietary data (Adobe) is stable. The company that rents its AI from the lab that just launched a competing design tool (Figma) is at a 52-week low. And the lab itself (Anthropic, $800 billion) is worth 19x more than all of them combined.

TASTEMAKER

Couchella weekend 2. Last week I talked about Couchella weekend, where my wife and I curl up on the couch and watch music all weekend long. Great news is that this is Weekend 2 so you can catch up on all the stuff you missed. Below were my top three sets from last week that you should catch:

Nine Inch Noize is UNBELIEVABLE. Watching the set I drooled. Convulsed. Exclaimed. The band’s industrial, thumping sound has literally never sounded better since they started in 1988. Frankly, I’ve never been all that into the original band of Nine Inch Nails, but this variation of it that incorporates German DJ Boys Noize, takes the music to a different dimension. Watch the band’s performance of Heresy if you need further convincing.

David Bryne. I am in year three of a Talking Heads obsession, so unsurprisingly, David Byrne’s effervescent joy still got me at Coachella. He is 73 years old and still showing how it is done. Check out Life During Wartime.

Katseye. Look, I am not a K-Pop guy. Just not my thing! But maybe its been my daughter’s obsession with K Pop Demon Hunters, but the genre has slowly been growing on me. I had a great time watching the all girl group play frantic beats to a screaming crowd. Check out Pinky Up.

Go and be kind this week,

Evan

Sponsorships

We are now accepting sponsors for the Q2 ‘26. If you are interested in reaching my audience of 34K+ founders, investors, and senior tech executives, send me an email at team@gettheleverage.com.

Excellent analysis of the stakes here. It's hard for me to imagine what an intelligence explosion will look like and I think we all have to go about our business assuming we have no ability to predict. Otherwise we'd just stay frozen.