The Most Aggressive Quarter in Capitalism

The Weekend Leverage, May 3rd

There were five Big Tech earnings calls this week with Microsoft, Alphabet, and Meta on Wednesday, Amazon and Apple on Thursday. After studying each of their quarters, the thing that has stuck with me through all of them isn’t any single line on any single P&L. It’s the shape of these companies. The revenue, the growth rates, the capex, the breadth of revenue lines, the willingness to bet the entire balance sheet on a technological wave that is barely two years old.

None of it has a real precedent in the history of capitalism. These are unusually intelligent, unusually successful, and unusually aggressive corporations, run by people who appear to be temperamentally incapable of letting a wave pass without trying to own it. Three things from this week stood out to me as a clean distillation of that posture — and three of the strategic challenges that come with it.

This week’s news was the kind that reinforced how different the world will be in five years. But first, this newsletter is brought to you by returning sponsor Bolt.

Here’s what’s actually happening inside your company: your PM built a dashboard in an AI tool last week. Marketing has gone rogue and is building hundreds of landing pages. And, unfortunately, absolutely none of it can ship, because none of it was built with what your engineers use.

Most AI coding tools try to solve this with a “design system.” Which really just means six hex codes and a font. That’s a decorative theme. It breaks the second a real engineer opens the file.

Bolt.new’s Design System Agent reads your real components from GitHub, Storybook, or npm. Every prototype uses your actual production code, not a re-skinned approximation. When engineering opens the file, it’s already there.

The prototype stops being throwaway. It becomes the thing you ship.

MY RESEARCH

Why is AI hiring seniors and firing juniors at the same time? On April 15, Snap fired 1,000 engineers and disclosed that 65% of new code is AI-generated. A week later, Sundar Pichai admitted Google is at 75%, up from 25% in late 2024. Yet aggregate engineering postings just hit a multi-year high, with senior roles up and junior dev postings down 67%. Employment for devs aged 22-25 has cratered 20% from its 2022 peak. What the hell is happening???? I built a benchmark comparing assembly, C, Python, and AI prompts to figure out which layers of the knowledge stack are about to disappear. Read here.

WHAT MATTERED THIS WEEK?

BIG CAPEX

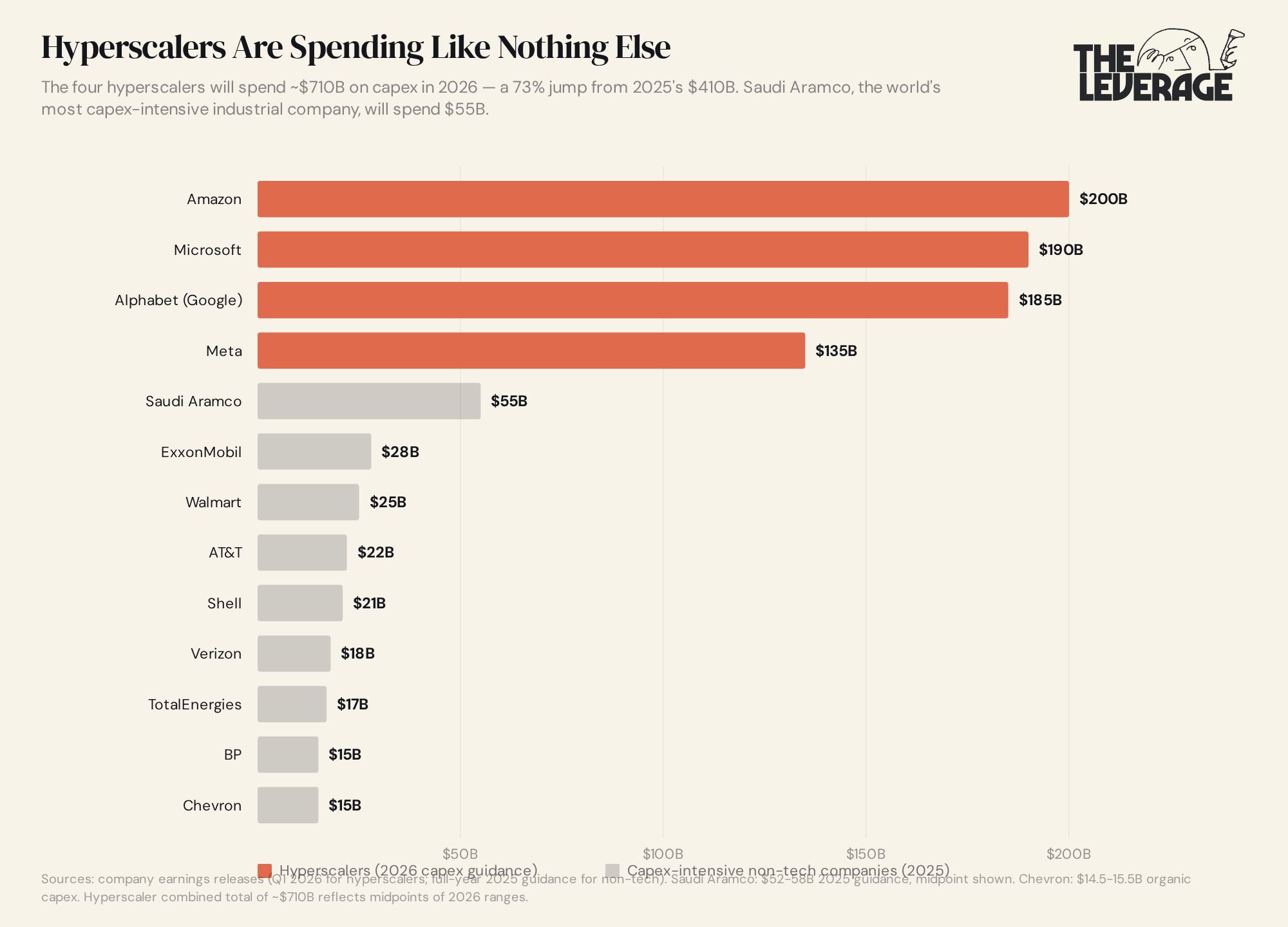

Datacenter money printer go brrrrrr. The capex numbers from this week are large enough to make you go numb. Microsoft put up $31.9B, up 49% YoY, on the way to roughly $190B for calendar 2026. Amazon hit $43.2B in Q1 on its way to a guided $200B for the year. On Wednesday, Alphabet and Meta walked onto their earnings calls and raised their 2026 capex ranges. Alphabet bumped its range from $175-185B to $180-190B and warned that 2027 would go meaningfully higher; Meta raised from $115-135B to $125-145B and watched its stock fall 7% in the after-hours for the trouble.

People typically cite stuff like the Manhattan project or other large scale government projects to help people grok the amount of cash being incinerated. However, the right comparison is the most capex-intensive companies on the planet. Saudi Aramco — the entity that physically pulls every fifth barrel of crude out of the ground globally — is guiding to $52-58B for 2025. ExxonMobil is closer to $25B. Amazon is spending nearly 4x what Aramco spends to maintain the world’s oil supply. The company that sells you diapers is now the most aggressive industrial spender in the history of capitalism.

Beyond the eye popping numbers, what strikes me is the level of aggressiveness. By every textbook of corporate strategy, dominant incumbents are supposed to defend. When you’ve reached the kind of category dominance and share of national market cap these companies hold, the historical default is to protect the golden goose. IBM sat on mainframes through the 1980s while the PC era began, then watched the value migrate up the stack to an OS it had licensed away. Kodak invented the digital camera and then chose to defend film. Microsoft itself, under Ballmer, sat on Windows and Office through the 2000s and missed mobile, missed search, and very nearly missed cloud. Each of those companies, at its peak, sat at a comparable share of sector revenue to where Microsoft or Alphabet sit today. Each chose to defend their territory. Each lost.

Big tech CEOs were handed unbelievable strategic advantages with their companies, but in contrast with prior generations of C-suites, has continued to act like founders. They are the first cohort of dominant tech incumbents in modern memory to bet the existing engine on the next one. Amazon’s trailing twelve-month free cash flow has collapsed 95% to $1.2B because of AI capex. Meta absorbed a 7% drawdown to do the same on Wednesday. Alphabet pre-warned the market that 2027 will get worse before it gets better.

I find the scope of ambition is bracing. These companies are running their balance sheets the way a venture-backed startup runs its Series B — burn now, win later, refuse on principle to let any technological wave pass without trying to own it. Whether the bet pays off or not, it’s not the bet a normal dominant incumbent would make.

BIG GROWTH

Big Tech is growing at the rate of series A startups. In a normal business, the bigger you are, the slower you grow. Once your company is doing $300B+ a year in revenue, the entire economy is too small to grow into. The biggest companies of every previous era followed the rule. Walmart at peak grew in the low double digits. ExxonMobil’s best year as a megacap was around 8%.

Big Tech once again has defied history.

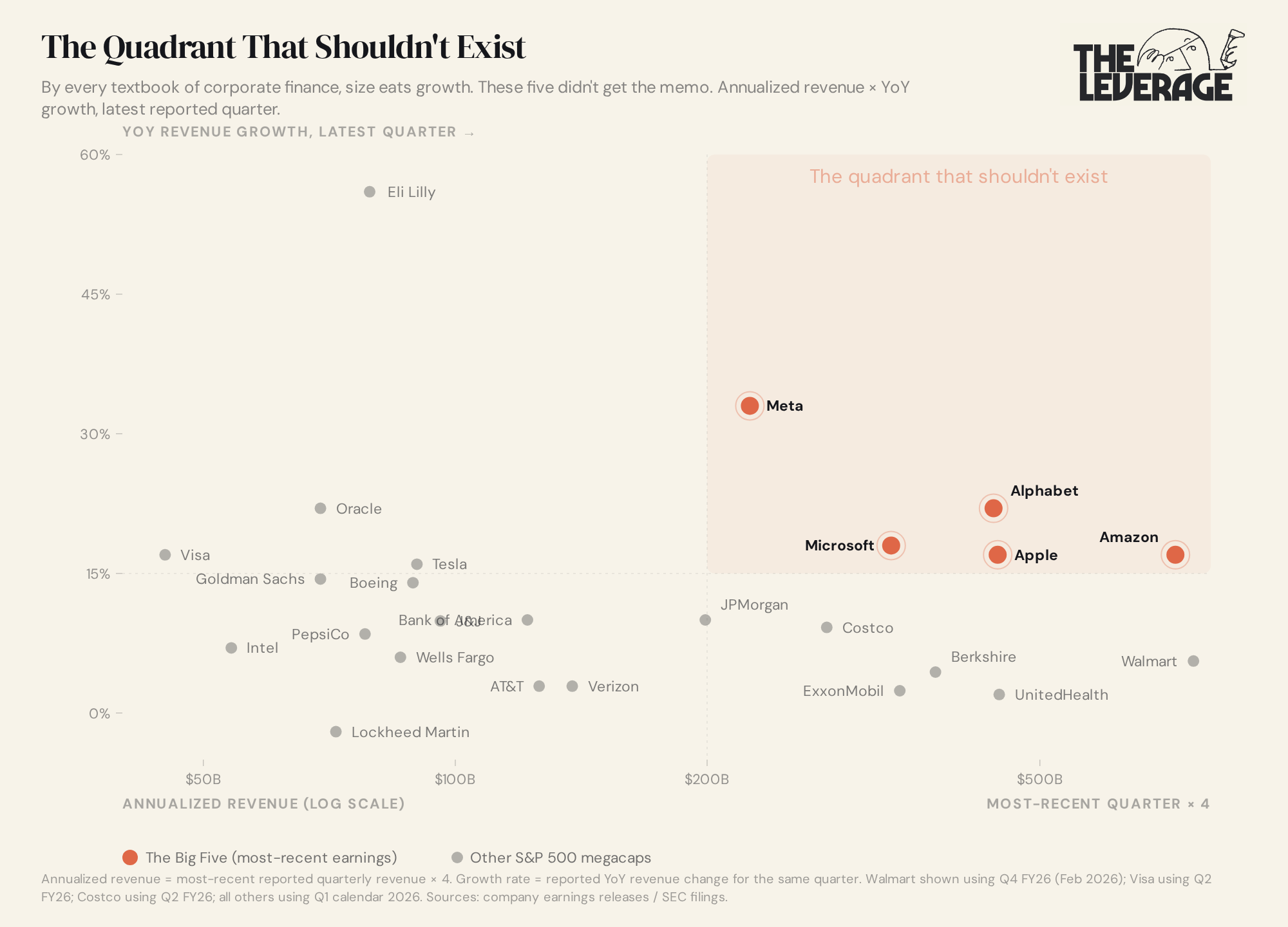

Meta did $56.3B in revenue, up 33% on a $225B annualized base. Alphabet did $109.9B, up 22% — its fastest growth quarter since 2022 — on a $440B base. Microsoft did $82.9B, up 18% on a $330B base, with Azure alone running at +40%. Apple did $111.2B, up 17% on a $445B base. Amazon did $181.5B, up 17% on a $725B base, with AWS reaccelerating to 28% — its fastest growth in three years.

For comparison, the median S&P 500 large-cap grew low-to-mid single digits over the same period. Three of these five companies post higher annual revenue than the entire economy of Portugal, and they are still growing faster than the average $50M Series A startup.

I pulled the most-recent-quarter revenue for 25 of the largest companies in the S&P 500. From there, I annualized their revenue, tossed it on a log scale, and plotted the growth rate for the entire set. The entire bottom-right of the chart is what the textbook says should happen at this size, and the upper-right is where the Big Five are quietly relocated.

The growth-at-scale assumption — that megacaps slow down because there’s nowhere left to expand into — is functionally dead.

BIG DISTRACTION

The companies also face strategic champagne problems. Beyond the raw numbers, these companies have gotten so large on their core strategic advantages that it is possible that their new business lines become more important then their marquee products.

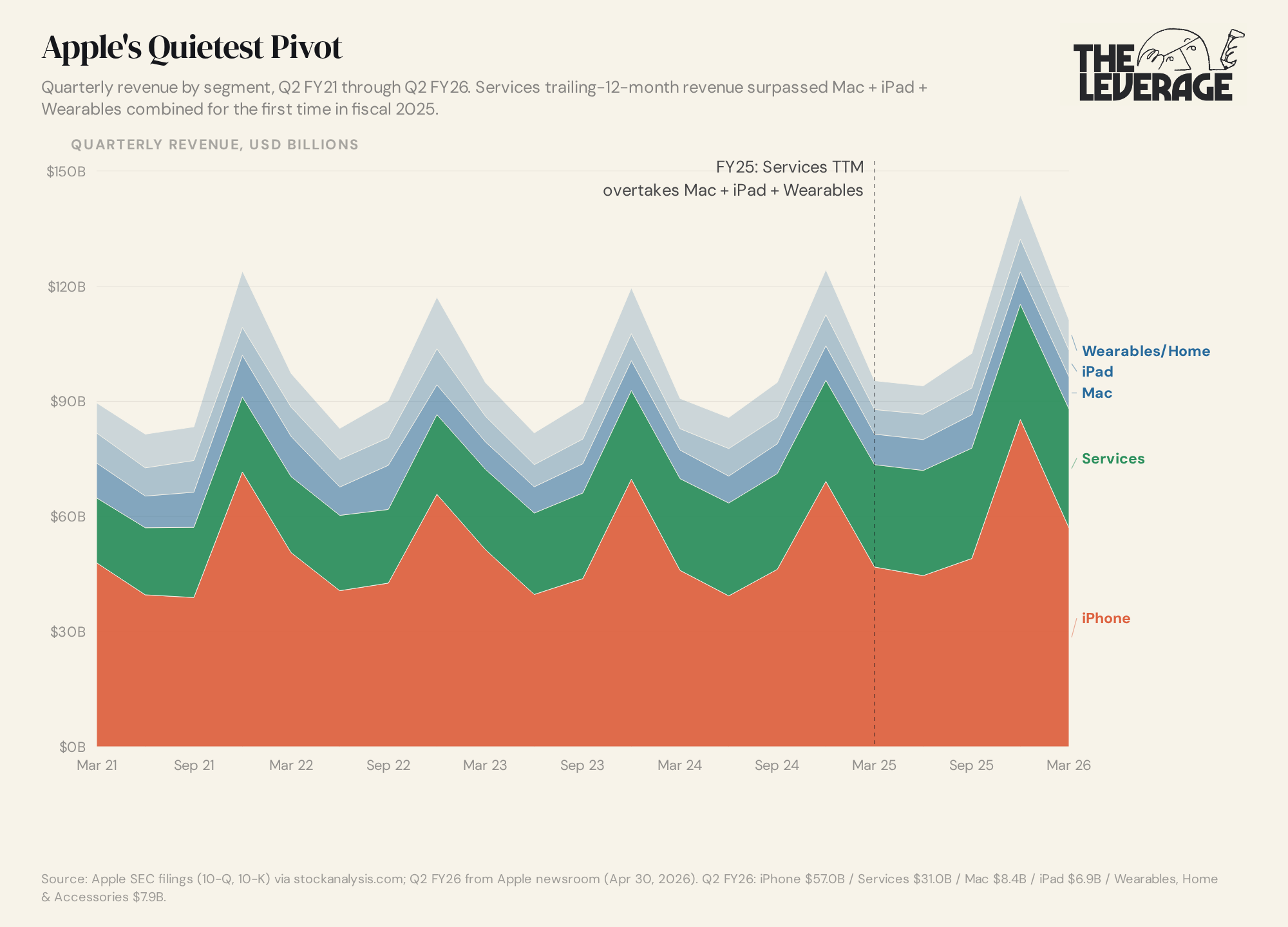

No company is a better example of this then Apple. Their Q2 FY26 segment breakdown is the most strategically interesting line item in the entire week. iPhone at $57B (+22%). Services at $31B (+16%) — an all-time high. Mac at $8.4B (+6%). iPad at $6.9B (+8%). Wearables, Home and Accessories at $7.9B (+5%). Services is now bigger than Mac, iPad, and Wearables combined ($23B). It is unambiguously the second pillar of the company.

I plotted Apple’s quarterly revenue segment over the last five fiscal years. The iPhone is still the largest segment, but the dashed line at fiscal 2025 marks the moment Services trailing-twelve-month revenue passed Mac, iPad, and Wearables combined for the first time, and the gap has only widened since.

The Services division is kind of a grab bag of everything that doesn’t require hardware. You have the 30% App Store cut on in-app digital purchases, Apple Music, iCloud storage subscriptions, Apple TV+, AppleCare, and Apple Pay. But wait! There’s more random shit. Search engine licensing fees from Google which is roughly $20B/year of nearly pure-margin revenue. There’s advertising in the App Store. Apple Arcade, Fitness+, News+. Almost all of this revenue is gross-margin-rich with the segment running at north of 70% gross margin. This is about twice what the hardware delivers. On paper, it is the most attractive line of revenue in the building.

It is unfortunately, strategically evil.

Apple’s corporate power has never and will never come from Services. It comes from the iPhone — and from Apple Silicon, the M-series and A-series chips that have made Apple’s hardware the best-positioned consumer platform for the AI era. Services is a derivative business. It is not an independent one.

If you gave 99% of CEOs this type of business line, they wouldn’t be able to stop themselves from gorging themselves on it. It’s like putting two bowls in front of a dog — one full of steak, one full of vet recommended kibble — and trusting it not to eat the steak till they throw up. Every quarter the App Store fee structure tightens, every additional ad slot inside iOS, every nag screen pushing iCloud, every redirect to Apple Pay are immediate revenue wins for Cupertino. They also compound, slowly, into the kind of friction that makes the iPhone meaningfully worse to use. I’ve certainly felt this over the last five years. There are a variety of enshittification moments with iPhones now. My latest was my brother in law texting me an Apple Music link which led to Apple inserting an ad into iMessage. This is evil and sucks and probably quite profitable.

The risk is that Apple enshittifies the iPhone in the pursuit of more Services revenue, until enough users notice that the once helpful tool becomes a toll booth. Each of the members of big tech has some temptation like this, where if they let themselves have sloppy management, they could slowly erode their core competitive advantage. For this quarter at least, all of them hav resisted that temptation.

TASTEMAKER

The sacrifice at the summit. This is my first time reading Kierkegaard, and the defining attribute of his book Fear and Trembling is its staggering beauty. The ~100 page book is about the Biblical story of Abraham being commanded by God to sacrifice his son Isaac. Kierkegaard spends the book turning that single moment over and over and over. He asks what faith actually requires of a person. If you follow one of the Abrahamic religions you can interpret that your own belief system, but it struck me as a larger concept as a parent and a founder.

But man, the prose. Sentence after sentence, layer after layer of the sublime writing does work that almost no contemporary author even attempts. Abraham is ultimately a figure of paradoxes, and Kierkegaard keeps pointing those out until the absurdity of belief starts feeling like a thing you can almost touch. Highly recommend, especially if you want to sit with the nature of faith, the attempt to climb the mountain, and the absurdity of believing something back into existence after you have given it up.

Go and be kind this week,

Evan

Sponsorships

We are now accepting sponsors for the Q2 ‘26. If you are interested in reaching my audience of 34K+ founders, investors, and senior tech executives, send me an email at team@gettheleverage.com.

Love that you got a shout out from Rory on the weekly 20VC this week! That was cool especially so soon on the heels of your very candid and really impactful writing about where the business and you were a few months ago. I've been there (a few times) but you are doing something special and differentiated so glad you persevered!

Incredible newsletter, wonderful insights. Lot of food for thoughts in the weekly issue.