Should Meta Let Drug Dealers Buy Ads?

The Weekend Leverage, November 9th

Hi everyone, I recorded some of my best episodes ever this week and put the final touches on research reports that have taken months of interviews to put together. Keep an eye on your inbox over the next few days, there is gonna be a spicy amount of takes from The Leverage.

This edition we’ll cover:

Doordash’s cute robot that cost them 20 billion dollars in valuation.

Why Meta isn’t banning scam ads, only charging them higher prices

3 new academic papers on economics and social media blew my mind

MY RESEARCH

Should your company convert to Christianity? Before networked computers, companies often aspired to build geographic monopolies. In the AI era, companies are attempting to build theological monopolies instead. By being the company that captures the economic value of a belief system, you can build a differentiated profit margin. This research report looks at two IPOs this year that try to build Netflix for Christians and Vertical SaaS for churches. I think it is likely that more firms will try to lean hard into identity politics as distribution becomes ever more competitive. Read more here.

WHAT MATTERED THIS WEEK?

PUBLICS

DoorDash stock dropped 20% because they are making the right choices. The burrito-taxi company announced a plan to spend ““several hundred million dollars more” in 2026 to support their highly ambitious product roadmap. The market hated this. Huge selloff. Blood curdling screams echoing throughout Wall Street, etc etc.

The company currently operates in a competitive oligopoly in the U.S. with their international expansion clearly charting towards a similar end state. Uber is almost always around and never lacks the ambition or network effects to compete with DoorDash. To prepare for this globally competitive inevitability, DoorDash management has taken one of the most aggressive expansions I’ve seen from a public company. They simultaneously executed a $1.2 billion acquisition to extend deeper into Vertical SaaS for restaurants, acquired a large European delivery player for $3.9 billion, and announced a new delivery robot a few weeks ago.

In contrast with Wall Street however, I believe the company is investing appropriately (and should perhaps be more aggressive).

This increased spend made me think of a new paper “Algorithmic Predation: Equilibrium Analysis in Dynamic Oligopolies with Smooth Market Sharing,” which uses deep reinforcement learning to show that price wars only make sense when you own a structural cost advantage (especially when rival exit is plausible). That’s the DoorDash read: they’ve landed in oligopolies with well-funded competitors. While they could slash prices to grow, as they did in the early innings of the delivery market game, that ends up helping no one. The paper’s point is you win price wars only if your cost curve is lower—so Doordash invests now to change the cost structure (global platform to unite their delivery acquisition, robotic autonomy to have hardware other firms can’t match, and retailer/vertical-SaaS rails to increase merchant lock in) and earn the right to subsidize later without lighting cash on fire.

As founder/CEO Tony Xu put it: “We wish there was a way to grow a baby into an adult without investment… but we do not believe this is how life or business works,” and the payoff is a single global platform that “will allow us to not only have a better cost structure, but… do a better job in solving the next problem for customers.”

I’ve been talking with various members of their leadership team over the last month and will have an updated deep dive on the company this week. Make sure to upgrade to a paid subscription to receive it in your inbox.

10.1% of Meta’s ads are scams (and that could be ok?). According to reporting based on internal documents obtained by Reuters, Meta earned over $7 billion in 2024 from ads that could be deemed as “scams” or other higher risk categories like false medical information, gambling, illicit goods, etc. To combat these types of advertisers, the company has a two-fold system.

“The company only bans advertisers if its automated systems predict the marketers are at least 95% certain to be committing fraud, the documents show. If the company is less certain – but still believes the advertiser is a likely scammer – Meta charges higher ad rates as a penalty.”

Frankly, reading this paragraph Meta feels a little ghoulish. Because such a high percentage of the ads are scams, if the company banned all the accounts overnight that they suspected, a 10% drop in revenue would seriously harm Meta’s valuation. The “higher ad rates” as a suspected scam penalty is an elegant solution only in that it allows Meta to retain revenue while reducing scams. However, this cost ends up being borne by the consumer being defrauded, and by the other advertisers on the platform who end up having to compete in ad auctions with Nigerian scammers whose profit margins are structurally higher—there are not a lot of structural costs in ye olde stealing business. The company only became more aggressive against scams in regions with pending regulatory action, where the fines for their failure to regulate outstripped the profit Meta could derive. Not great!

To steelman the counter-argument: The optimal number of fraud on an ads platform is not zero. if you run an ad machine at incomprehensible scale, even a teeny false-positive rate means you accidentally kneecap a lot of real small businesses, so you set a high ban-with-confidence number, which is the 95% that their system uses to ban, and then triage. Where you’re less sure, you don’t nuke the buyer, you make them pay more—a kind of “sketchiness surcharge”—which both throttles their reach and funds better filters. From there you chase the fattest tails (impersonations, financial scams) and ship systemic fixes rather than sprinting after every noisy user report. Also, broad over-blocking creates its own legal/commerce/speech mess—especially for weird-but-legit SMBs—so sticking to clear, letter-of-policy rules until regulators finish writing the rules is, if not heroic, at least sensible.

Whether something is a “scam” or just a risky ad category is a matter of definition. But in response to Reuters, Meta’s comms staff said the 10.1% number was “rough and overly-inclusive,” but then refused to give the current number of estimated scams, how they define those scams, or how much they were investing in countering those scams. Worse, the KPI for the scam team wasn’t consumer harm, but harm to Meta’s revenue growth in 2025. “The team responsible for vetting questionable advertisers wasn’t allowed to take actions that could cost Meta more than 0.15% of the company’s total revenue” according to Reuter’s reporting. All these facts together indicate to me a company that is aware of scams and believes it is too powerful and too opaque to be forced to sacrifice significant revenue to protect consumers. Meta has a documented history of doing logically reasonable, but morally dubious ad policies, and this latest report seems to show that culture has metastasized within the organization. I find myself doubting that Meta deserves the benefit of the doubt.

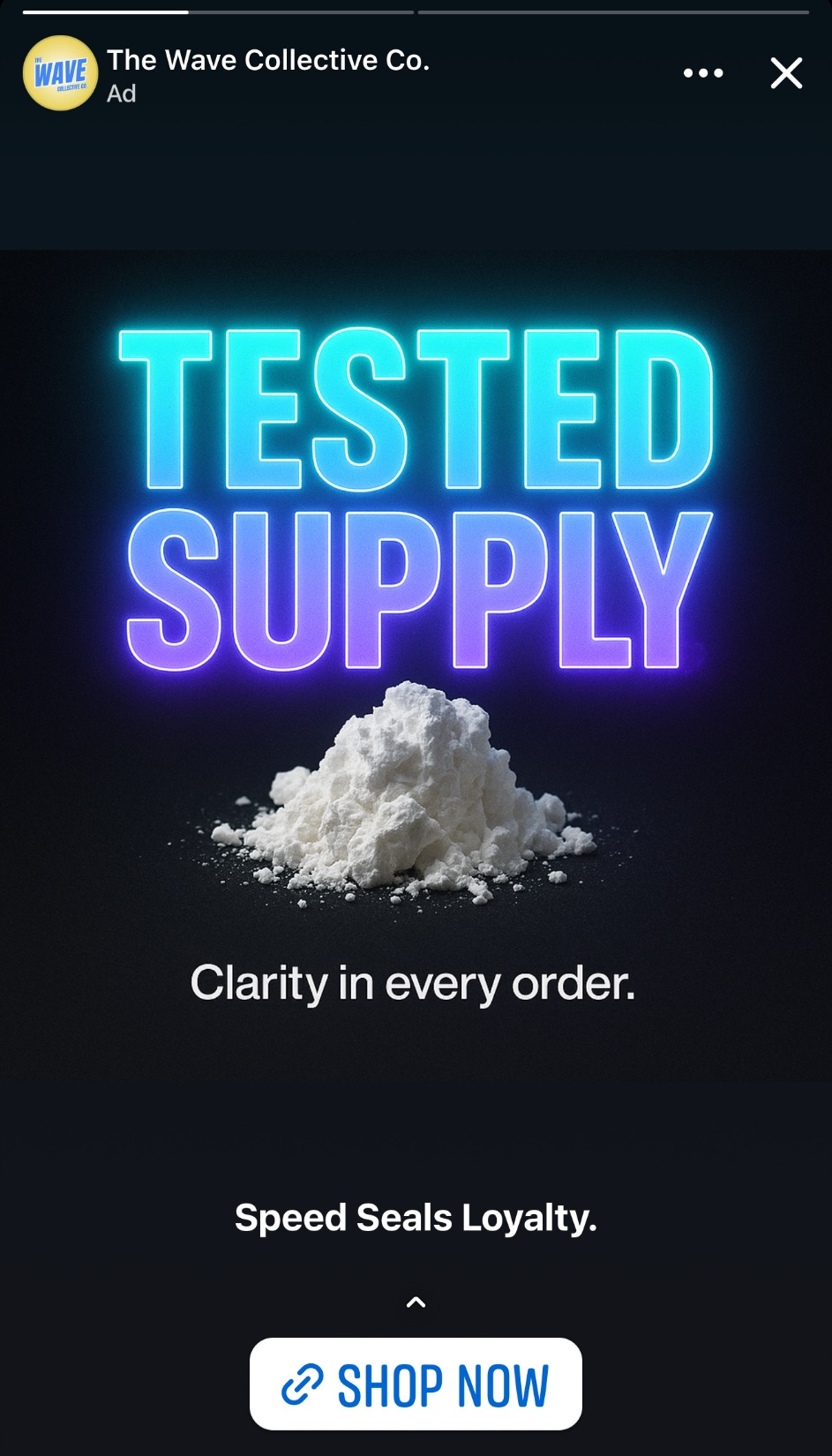

For an example of what these scams look like, here is a recent example of a drug dealer advertising cocaine on Instagram. You can even browse that advertiser’s website—which, somewhat hilariously, is incredibly well-designed and uses many UX patterns that are considered best practices in the ecommerce industry.

AI LABS

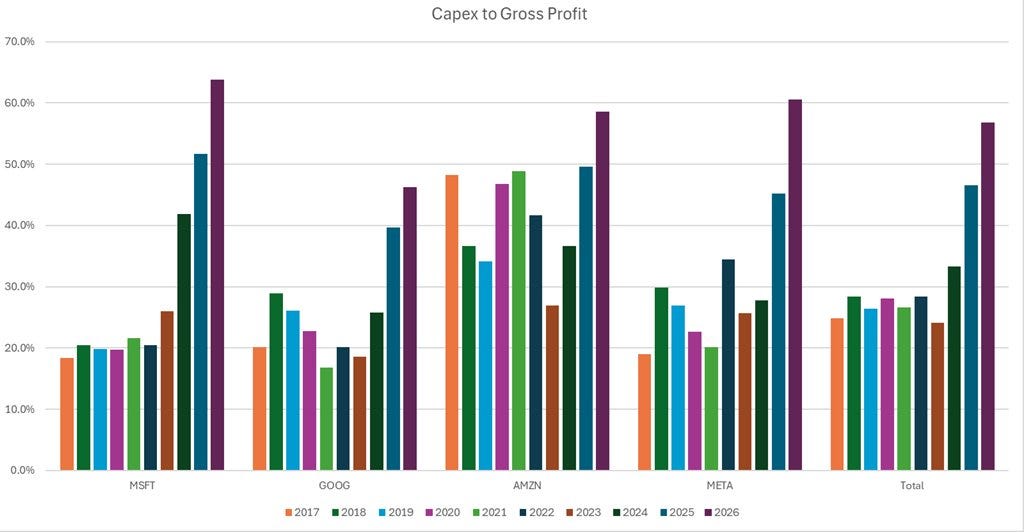

The data center spend looks reasonable for most of big tech. The last two years have seen a dramatic escalation in capital being spent for big tech to build out datacenters. X account modest proposal comments that “MSFT and META now are over 60%. Without an external facing cloud business (yet?), META is spending at or above the levels of the big 3 clouds. Capital intensity for the group is now up from an average of 27% (’17-’22) to 57%...If you take 2026 capex, and compare it to what each would be spending if capital intensity remained flat with the average pre-AI, it’s around $292.9B extra.” To accompany that analysis, that account shared this chart.

It’s tempting to look at this image and go full Jar-Jar Binks levels of insight, “ah number go big bad but directly attributable revenue got not big, so dis bery concerning.” Do not fall prey to this temptation. An additional $300B in spend is reasonable because the GPUs staffing these data centers can be rented to other applications (Microsoft, Google, Amazon) or can be utilized for other applications of machine learning like ad targeting or ad generation (Meta + all of our previous players).

The long-term justification for these datacenters come not from attributable revenue, but improved operations. Some nerdy, bespectacled analyst is locked in a windowless closet at each of these companies trying to calculate the most profitable use of these GPUs, not whether they will be used at all. For more on this math, and on how it works in the contexts of ads, see my research report here.

SMART PAPERS

Social media rots every mind it touches—silicon or squishy. On the machine side, LLMs Can Get ‘Brain Rot shows that continually feeding models high-engagement, low-quality social content causes a dose-response decline in reasoning, memory, and safety—and that later “clean” finetuning only partially heals the damage. Simultaneously on the human side, “Estimating the effect size of moral contagion in online networks: A pre-registered replication and meta-analysis” nails a complementary point that for each additional moral-emotional word in a post, the expected number of shares was 13% greater. This has been something any creator could’ve told you, but it is good to have science backing up that intuition.

I am growing increasingly convinced that it is the inherent nature of social media to corrupt our minds. It is not an issue of “AI slop” or evil creators or anything else, the rot of social media is baked into its existence. There is a real opportunity for a creator or a company to position itself as the anti-rot, anti-slop platform. Maybe this is a venture scale opportunity for me to build or to help fund. Please reach out if you are a founder addressing this problem.

TASTEMAKER

We are officially in the awards season for film! Lots of great movies to go see right now. Over the next few weeks, I’ll tell you which ones are worth checking out and likely award nominees.

Frankenstein (Netflix and select theaters): From director Guillermo del Toro, this 2-hour-and-29-minute film is a film of contrasts. At certain points it hits the highest of highs, from actor Jacob Elordi’s sensitive portrayal of the monster to some of the most incredible set and costuming designs I’ve ever seen. On the other hand, this film’s script has all the subtlety of a punch in the face. There were multiple line reads that were so bad I physically shuddered in my seat. This won’t work for everyone, but I saw it in 35mm with a sold-out crowd on the weekend before Halloween, and from a visual perspective, feasted. Recommended if you enjoy gothic horror and don’t want to think too hard. See it in theaters if you can, it’ll be much better that way! (This is always true, but it is especially true for this film). Expect nominations for Jacob Elordi, costuming, set design, and potentially even best picture.

A House of Dynamite: A remarkable first act that had my palms sweating, outright fails its promise in the second and third acts. Director Kathryn Bigelow (The Hurt Locker, Point Break, Zero Dark Thirty) uses a repeated time-loop narrative structure to show different perspectives of what would happen during a nuclear attack on America. That sounds great, except that we just watch the same Zoom call from like 6 different perspectives. Only Rebecca Ferguson’s character is believable/likeable and there are multiple, pointless plot lines. I was so disappointed by this one. Skip unless you long for films that show what a semi-competent federal government would look like. Long shot for Ferguson to receive an acting nod, but I doubt it.

This week I’ll be watching Bugonia and Sentimental Value and will report back!

Have a great week,

Evan

Sponsorships

We are now accepting sponsors for the Q1 ‘26. If you are interested in reaching my audience of 35K+ founders, investors, and senior tech executives, send me an email at team@gettheleverage.com.