Buy It, Gut It, Hold It Forever?

Bending Spoons is now a $25 billion public company. Its model raises interesting (and profitable) questions.

Bending Spoons rules the land of broken software toys. Over the last 10 years they’ve bought companies like Evernote, Vimeo, WeTransfer, Eventbrite, and, as of January, AOL. They run what is essentially a private equity version of Elon’s Twitter takeover playbook: buy legacy assets that are poorly managed, lay off all the staff, raise prices on existing customers, and then milk that cash cow till she runs dry. Importantly, the goal is to “hold it forever.” They are not trying to fix these things up to resell; they have built their model to keep their acquisitions on life support for as long as possible. They have acquired 50 businesses with this idea.

So far, they have been enormously rewarded for it. The IPO that happened this week came in above the $26–28 range it floated, which puts the whole thing somewhere around $19–20 billion. Two years ago, it was $2.8 billion. It finished its first day of trading at a $25.7 billion valuation.

So, naturally, it is worth asking: is this whole thing kinda stupid?

If you believe, as I do, that AI dramatically reduces the cost of creating software, wouldn’t a company whose whole identity is “we make software more expensive” naturally be a dud? A defensible version of this model would be to run a rollup. Bending Spoons could acquire companies that serve an important market, combine the disparate solutions into a superplatform, and then accumulate market share. That’s not what is happening. Instead, they are just kinda acquiring random software stuff that was famous and is now dead in the water. There is no strategic importance to having these assets held by the same company. Instead, the rationalization for Bending Spoons to own these things is some techstack synergies around pricing/advertising and then they get to bring in their team which is supposedly better than everyone else.

Therefore, to understand if this thing is stupid, we have to answer 3 key questions:

Is the company actually pulling this off? Is it working?

Is Bending Spoons the right corporate structure for this playbook?

Does AI make this thing go to zero?

Let’s talk about it.

1. Is it actually working?

At first glance, this thing looks impressive. Evernote is a clear case study of when it goes right. After the Jan 2023 acquisition, Bending Spoons cut the team by 82%, rebuilt the monolith into microservices, raised release velocity, and dragged it to the highest retention in the portfolio. Another example is Remini, a photo editing app. It was rebuilt from scratch, and now does 5x the users and 9x the revenue of its pre-acquisition self. These are genuinely great numbers!

If you don’t look too closely, the top-line numbers are also impressive sounding. Revenue went from $387 million in 2023 to $1.31 billion in 2025. Adjusted operating margin is 47% and climbing. Revenue per employee is $2.57 million, one of the highest figures in non-AI native software. This is all run by a central team so selective it hired 286 people out of roughly 800,000 applicants last year, a 0.04% acceptance rate. I’ve met several of their employees over the last two years and have always been impressed with their caliber.

Still, as always with tech stocks, the most important numbers are more challenging to find. Once I dug into their IPO documents, a clearer picture of the company emerged. If you stripped out the revenue that new acquisitions added, organic growth in 2025 was a measly 13%, and 7% in 2024. So of those 95 points of growth, roughly 82 were bought and 13 were built.

Blended net revenue retention is 94%, so basically the installed user base is actively shrinking, while new price increases are the revenue refilling the bucket. Evernote’s top tier has climbed from $110 a year to $250 since the acquisition, about 26% compounded. A good chunk of that “organic growth” is the sound of a shrinking base being charged more per head, faster than it churns.

This is a deliberate strategy by our friends in Milan. They mostly refuse to do paid acquisition and in 2025, 79% of revenue from new customers came through organic channels like word of mouth. They deliberately favor targets that don’t lean on paid acquisition, because paid demand is volatile and they want revenue they can forecast years out.

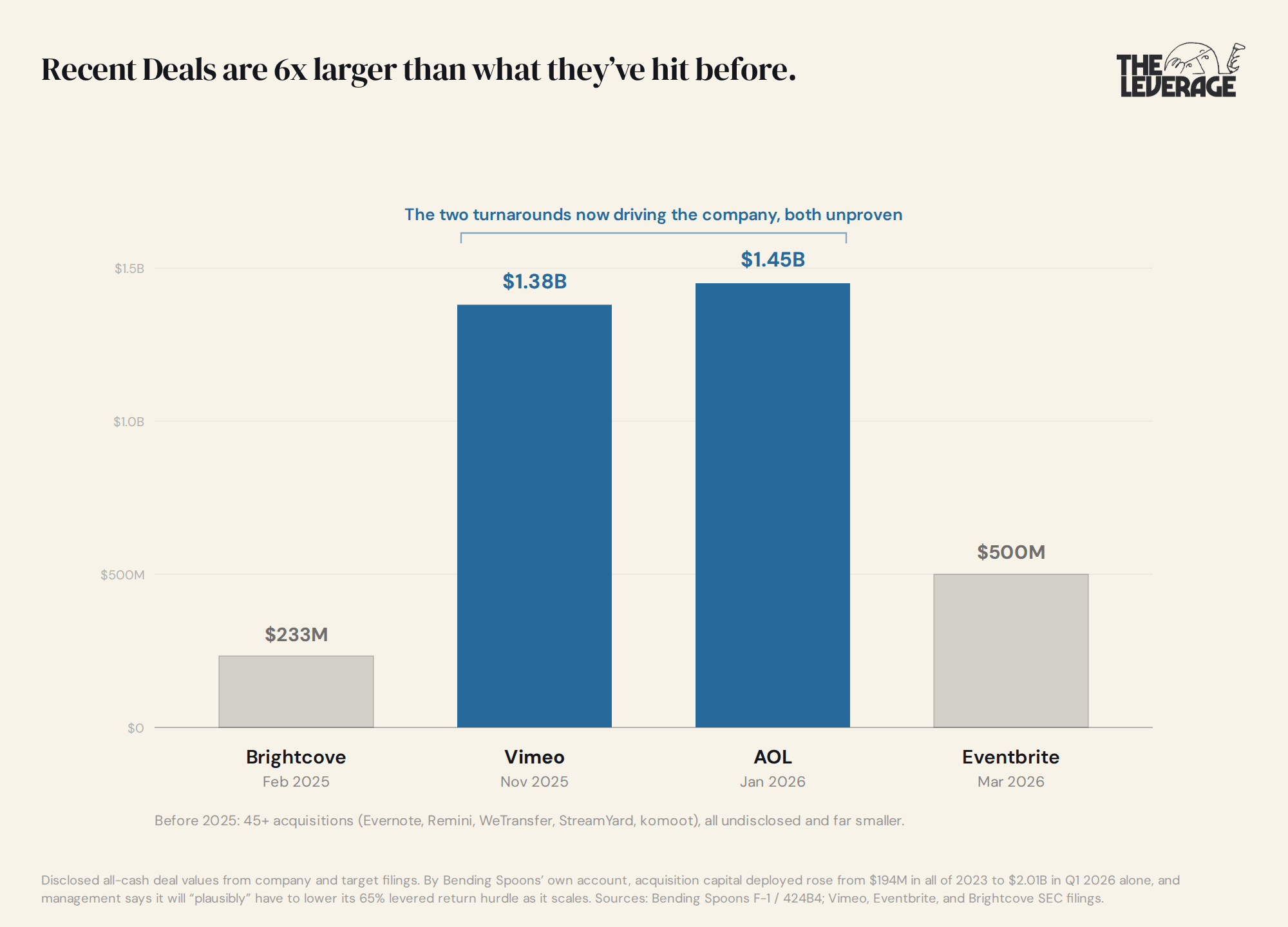

So is it working? From the numbers we can see, yes. However, the company doesn’t give any cohort analysis, no ROIC measurements on each individual deal, really anything I would look for if they approached me to invest in the company when it was private. To make it worse, over the last few years the size of the deals they are doing has dramatically escalated.

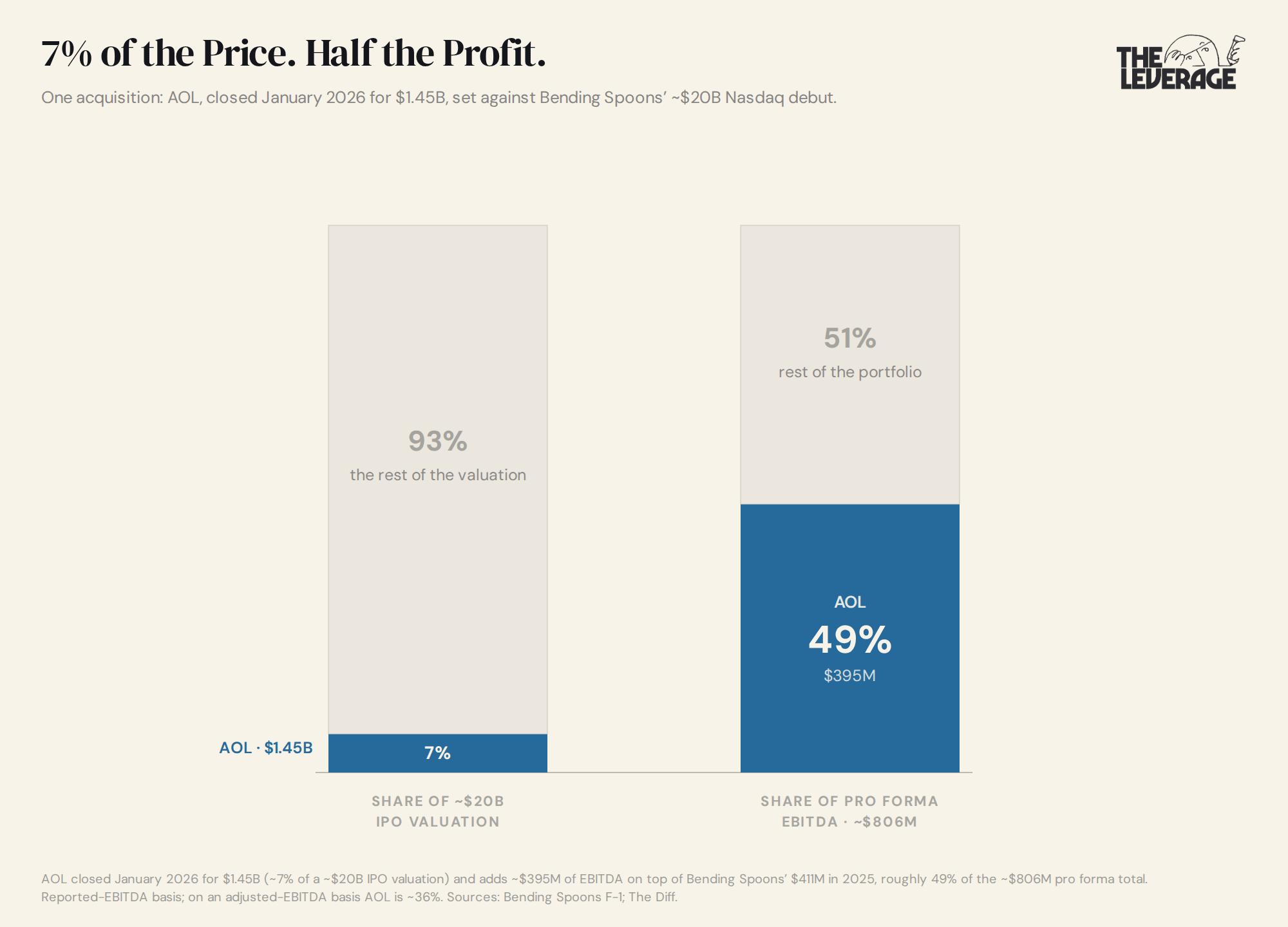

For most of its history, the deals were small. Then, in the span of about a year, they wrote a $1.38 billion check for Vimeo and a $1.45 billion check for AOL. Those are each roughly 6x the size of Brightcove ($233 million), the biggest deal they had a public price tag for before that. By their own accounting, capital deployed on acquisitions went from $194 million in all of 2023 to $2.01 billion in the first quarter of 2026 alone. In the IPO docs, they even admit they will “plausibly” have to lower their return targets as they keep scaling. When an acquirer tells us its returns are about to get worse, maybe we should believe it?

AOL by itself is roughly half of revenue, which means one unproven integration is half the entire P&L, and both AOL and Vimeo are still mid-turnaround. Cutting a note-taking app down to 60 people is a genuinely different job than turning around something as big and sprawling as AOL. Maybe their magic will make the leap! These are clearly smart operators. But investors are being asked to underwrite the biggest, hardest, least-proven version of the model at the exact moment the stock price seems to assume the answer is a definite yes.

The deeper question for me is whether a buy-gut-hold-forever operation should be a public company at all.

2. Is Bending Spoons the right structure for this?

The best comparison for Bending Spoons is probably Constellation Software. Constellation acquires micro-vertical SaaS companies. It has compounded at about 35% a year for 20 years by buying software and never selling (sound familiar?) and for most of the last decade it traded at a fat premium, usually past 30x EBITDA.

This comparison didn’t even survive the IPO. Two things happened: The whole serial-acquirer category has re-rated, and Constellation now trades around 15x EBITDA, less than half its 2024 multiple. Meanwhile, Bending Spoons trades around 18-20x forward EBITDA, on a far more heavily adjusted EBITDA than Constellation reports.

On today’s numbers, the unproven, more-levered, higher-variance acquirer trades at a premium to the one with a 20-year record. Welcome to the AI frenzy.

Constellation suffered from the SaaSacre, where public market investors suddenly realized that software companies could be disrupted by AI. That worry has taken roughly half off Constellation from its highs. The company was rattled enough to hold a special investor call just to address AI during this period. Clearly, the market found the answers unsatisfying. Essentially for both of these companies, you are being asked to bet on this question: how long does old code generate new cash?

To my eyes, Constellation at least has a defense. Its portfolio is vertical software in niches where the customer is buying regulatory compliance, workflow lock-in, and a system of record. Customers aren’t going to be using vibecoded claudeslop to run their hospital billing systems anytime soon.

You may not believe that defense, but at least the idea exists. Bending Spoons has no such intellectual cushion. Evernote, WeTransfer, Eventbrite, and Vimeo are consumer and prosumer products with relatively thin switching costs.

All of this produces the strangest fact in this IPO. The market took the defended version of this trade, the one with 20 years of receipts and strategic moats, and cut it in half. Then it paid a premium multiple for the levered, consumer-exposed, unproven version of the same trade.

Either the market is wrong about software, or it is wrong about Bending Spoons. It cannot be right about both. Which story is right determines whether this is a generational buying opportunity or a handy way to incinerate your kid’s college fund.