Profit is for Chumps

AI startups should be increasing their spend

For venture-backed startups, the penalty for prudence is irrelevance. When you are dealing with markets that move as fast as AI, with investment capital that starts with a “Billi”, the worst thing you can be is slow.

Despite that, there has been a slew of negative reports detailing how AI wrapper startups like Cursor, Lovable, and Replit are running on thin margins (and sometimes negative gross margins). Or the takes dunking on how OpenAI could potentially lose $14 billion next year.

At the risk of this sounding off the absolute top of the bubble: It is entirely rational and correct to run negative gross margins as a tech startup in markets as dynamic as the current one. While these companies could easily start harvesting profits if they wanted to, doing so would be distinctly dumb. Profits are a sign that management can’t think of anything productive to do with their cash, other than making a tax donation to the federal government.

AI is perhaps the most exciting platform shift in computing history—if a founder can’t find a way to deploy excess cash flow now, when on earth can they?

Power over profits

Historically speaking, software companies justified investing lots of money upfront in service to long-term customer relations. Invest now, keep your net dollar retention (NDR) above 120%, and you could profit for a decade to come. The underlying financial logic was built on spending once, harvesting forever. Crucially, software companies couldn’t assume a dramatic reduction in cost. Bezos and the AWS boys were never going to send you an email saying they had magically reduced your expenses by 50%.

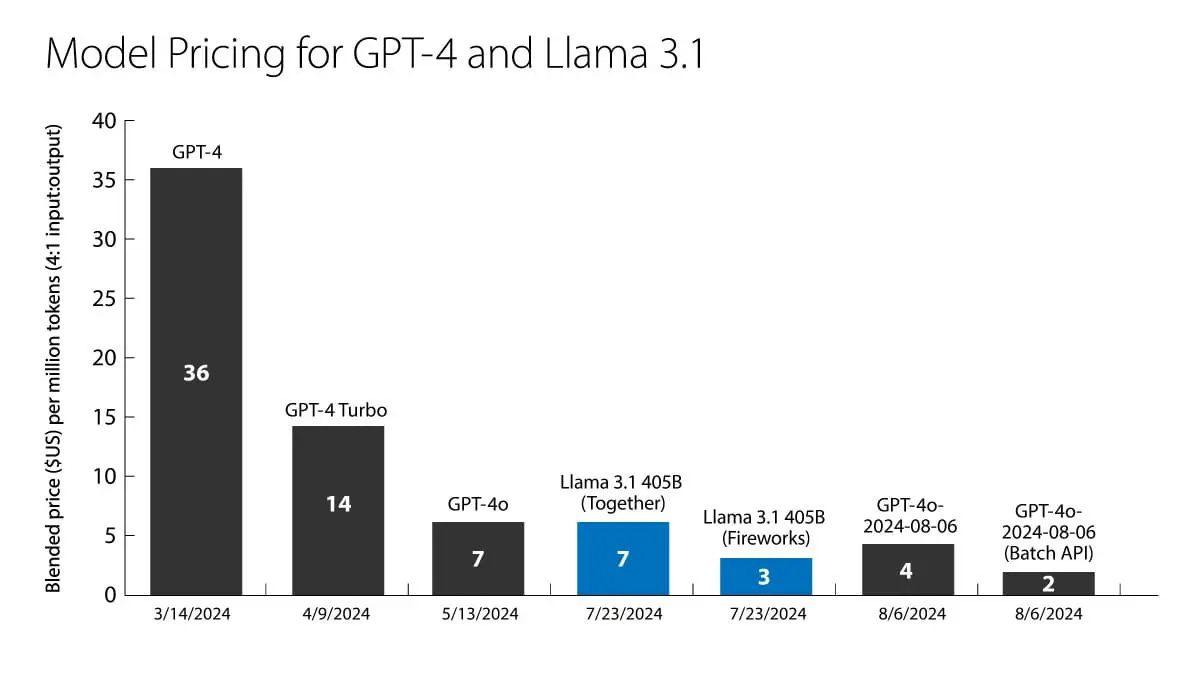

Generative AI is different. Every three to six months, foundation models companies like OpenAI will decrease your costs, increase your speed, and give you new, magical capabilities. Take, for example, just what happened with the GPT4 series of models. In just five months, you saw a ninefold decrease in your costs!

This dual quality—of decreased cost plus increased capability—fundamentally alters the economic logic of software startups. Negative gross margin now will be highly profitable in a year or two. Those new capabilities will allow software companies to capture new portions of its customers’ workflows. If you then price on a usage or outcome basis, that gives you a top-decile net dollar retention (NDR). It's not apples to apples, but Databricks is a major generative AI beneficiary and has a usage pricing model, and boasts of a NDR in the 140% range. Then, to improve margins you can switch customers to open-source models or models you train yourself.

Yesterday’s software companies subsidized account acquisition; AI companies now subsidize workflow acquisition. This slight tweak allows them to spend more on product today because they have the opportunity to capture additional labor spend tomorrow.

Cursor is the perfect example of this strategy. The company is one of the fastest growing application companies in history, scaling to well past $500 million in annualized recurring revenue. Its AI capabilities in the beginning were fairly standard, with features like autocompleting code. Each successive release added more AI quality, with an update in June focusing on adding in more AI agents. Simultaneously, the company is training its own models for the features it launched in 2023, while using GPT5 for its more frontier cases. This summer, they updated their pricing to be usage based (though not without some controversy).

Beyond following the path I laid out above, the non-intuitive lesson here is that the models weren’t the most important part. It was using the models to evolve the workflow of Cursor’s users. The goal of the company is to allow programming to occur in a wholly new way, not just to use AI. My suspicion is that use-case specific workflows, custom UI, and fine-tuned models are necessary to act as a total tool replacement for enterprise customers.

These tools are choosing to be unprofitable today to gain platform power tomorrow. However, this strategy is only possible with one additional counterparty: trigger happy venture capitalists.

Capital and market structures

In the first half of this year, VCs poured about $90 billion in North American AI startups. Capital is everywhere and it is coming at relatively low cost to founders. I frequently hear discussions of AI teams being able to raise at 50-100x revenue multiples or teams at the seed stage raising millions of dollars despite having zero customers. These types of multiples and risky bets have been present in Silicon Valley for over a decade; however, the capital base is just so much larger than in any previous era. Now, we have nations getting directly involved in investing in or subsidizing these companies. France goes to bat for Mistral. President Trump is live-negotiating deals with Nvidia. Saudi Arabia is building a data center big enough to host the Super Bowl.

But wait, there’s more money. Venture capital and private equity funds are sitting on $1.7 trillion in undeployed capital as of April of this year. On August 8, President Trump signed an executive order allowing people to invest their 401(k)s into private assets like crypto or private equity, even further exacerbating the too much capital problem.

There is a perfect storm of too much capital chasing after too few deals buoyed up by too much AI hype. Capital will never be cheaper, and as such, founders who have the fundraising gift can invest much more aggressively.

What ultimately matters

This is money poorly spent if it doesn’t form defensive moats. Relatively few AI companies have high switching costs or network effects. It’s why getting access to training data now is so important. It could be that typical workflow software is cheap (Cursor is hardly the only development environment), and the model too, is cheap (ChatGPT can write serviceable code for $20 a month), but combining the two is near impossible. These companies have to spend now so they can move beyond being just a wrapper.

And ultimately, profit doesn’t matter, cash flow does. This is not a new idea. In Jeff Bezos’ 2004 Amazon shareholder letter, he wrote, “Our ultimate financial measure, and the one we most want to drive over the long‑term, is free cash flow per share…When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.”

What is new is the scale of opportunity available. Usage-based pricing fundamentally alters the economic logic of software companies. If software companies continue getting cheap capital, then all signs point to spend.