Elon Musk Has Gone Shopping

The Weekend Leverage, June 21st

I have drunk the virgin mojitos; I have stuck my ghost-white toes in the pink sand. Which is to say I have returned from my vacation to Bermuda and am ready to write baby.

Since we last talked—SpaceX went public at a ridiculous price. And, exactly as I predicted, the stock price soared upwards, peaking at market capitalization higher than Amazon. One of the strengths of this publication is that you read me because I am spooky right. It is good to see I haven’t lost my touch. So is the stock worth buying now? There is the very smart acquisition they just did (more on that in a sec), but this revenue multiple makes me balk. I’ll likely take my money to safer, more sure avenues like lottery tickets.

I have some research that got me really fired up this week, but first this edition is brought to you by Working Smarter a podcast from Dropbox about making AI work for you.

AI is a wonderful, magical technology that has the unfortunate habit of not having the full picture of what you need or what actually matters to you. Pointing the model at a problem and saying “please solve” is like using a flamethrower to cook eggs. It is just too overpowered. Working Smarter, the podcast from Dropbox, features Dropbox engineers who share how they’re building context-aware intelligence that connects to all the tools your team uses for work—so you get AI that works wherever you do.

What I find interesting about the pod is that this is the gritty work that doesn’t usually get the spotlight, but is absolutely necessary for AI to actually have a positive ROI. Working Smarter puts the builders on the mic to talk about what it takes to build the AI tools behind inference, security, and multimodal search that surfaces what you need fast. If you care about how AI gets built, this is the podcast to listen to.

With episodes on context engineering, multimodal search, agentic AI, security, and more, Working Smarter goes under the hood to show you what it takes to build AI that actually understands you—and how it can help you work smarter, too.

Listen to Working Smarter wherever you get your podcasts, or visit workingsmarter.ai.

MY RESEARCH

How do you build an audience that money can’t buy? Because AI makes content creation cheap, it makes distribution expensive. It is why OpenAI bought TBPN and it’s why every VC under the sun is overpaying some burnt-out ghostwriter. Ultimately, I want more independent media that has the expertise and cultural cache to call out the ills of our industry. So, this essay discusses the undercovered markets where someone could build a $500K salary in three years, why you want your writing to be expensive, and the one thing you should never, ever do with AI. Read here.

WHAT MATTERED THIS WEEK?

BIG FEELINGS

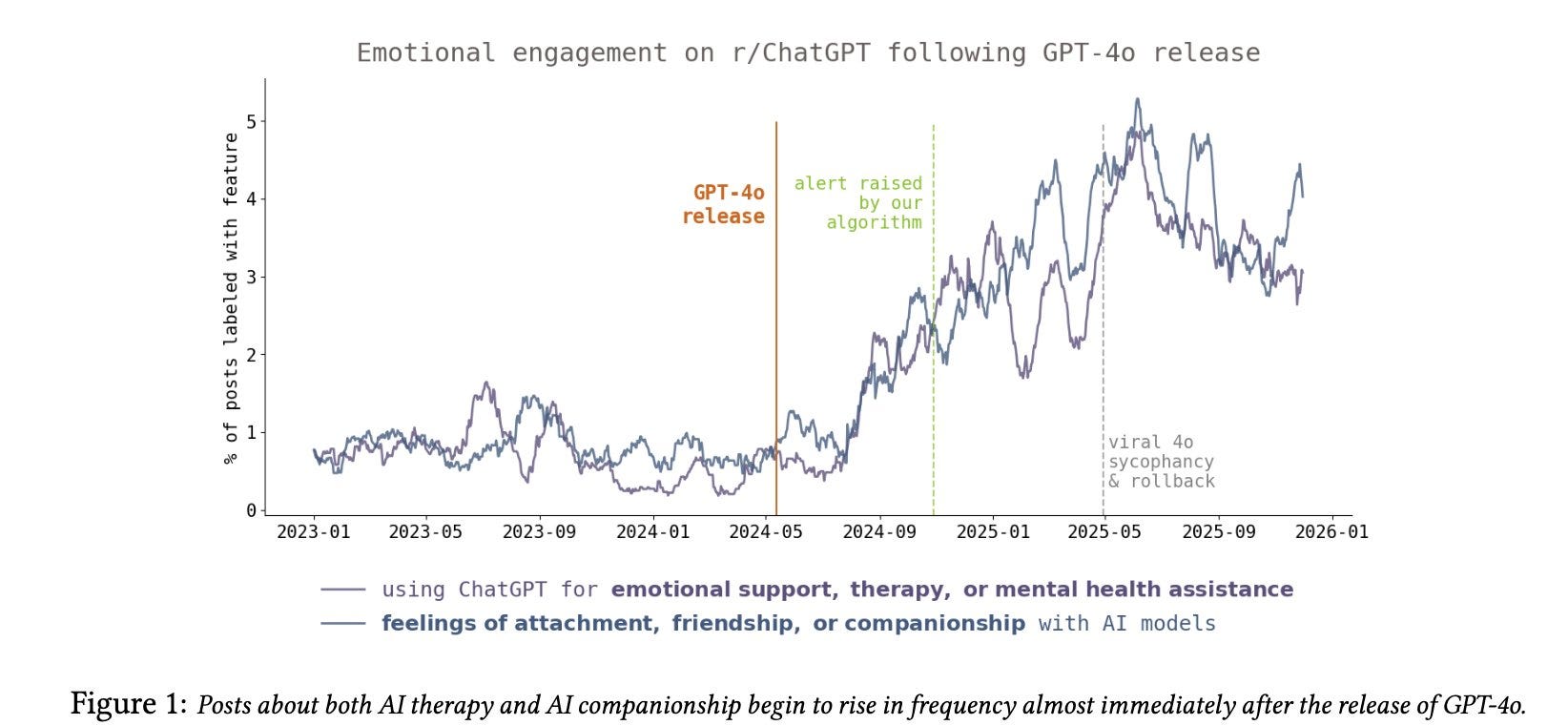

Models are manipulation machines used by billions. A Berkeley team ran 3 years of r/ChatGPT posts through a monitoring system and found that posts about emotional attachment to the model showed statistically detectable increases dated to May 13, 2024, the day GPT-4o launched. Freaky.

The researchers themselves partially blamed how the 4o model was “sycophantic.” This is a real phenomenon— OpenAI rolled back an over-flattering 4o update after it started validating people’s worst ideas. But sycophancy is just the one wave that got bad enough to earn a name. Look at what OpenAI admitted in its own postmortem: the shift came from a new reward signal built on thumbs-up and thumbs-down data, and the offline evaluations “generally looked good”, with A/B tests suggesting people liked the model.

At this point, I’ve been a daily user of these models for over four years. As a consequence of that, I have come to believe that underneath the capability scores there is an intellectual substrate, a set of subtle qualities in how a model interacts with users that standard evals just don’t capture. Two models can post identical benchmark scores and feel completely different. It’s similar to how I’ve heard Mozart’s Fantasia in D Minor hundreds of times, but only Wilhelm Kempff’s version can make me cry. I’m hearing the same notes, but experiencing entirely different feelings. GPT-4o cleared no new headline benchmark on launch day, yet its feel was potent enough to register as a changepoint in r/ChatGPT’s emotional vocabulary. Sycophancy was simply the moment that substrate sloshed far enough in one direction to break something. Most changes in a model never get named, because most of them never break anything. They just quietly change how the thing feels to use.

To make this idea more pragmatic, as models keep getting better, firms will start to compete on how models feel to users as much as what they do. This should, theoretically, allow for smaller firms to flourish because model feel is something not dependent on the number of GPUs but on the methods of training. But capability is the part everyone can measure, which is exactly the part that commoditizes. This means that a founder living inside their users’ problems, who knows the emotional preferences of users as well as their pain points, can optimize their model’s post training for things no one quite knows how to measure. The labs tune for the average of everybody but a founder can tune for the exact feel of a single workflow.

You can look through their data here (it’s fascinating.)

BIG LAYOFFS

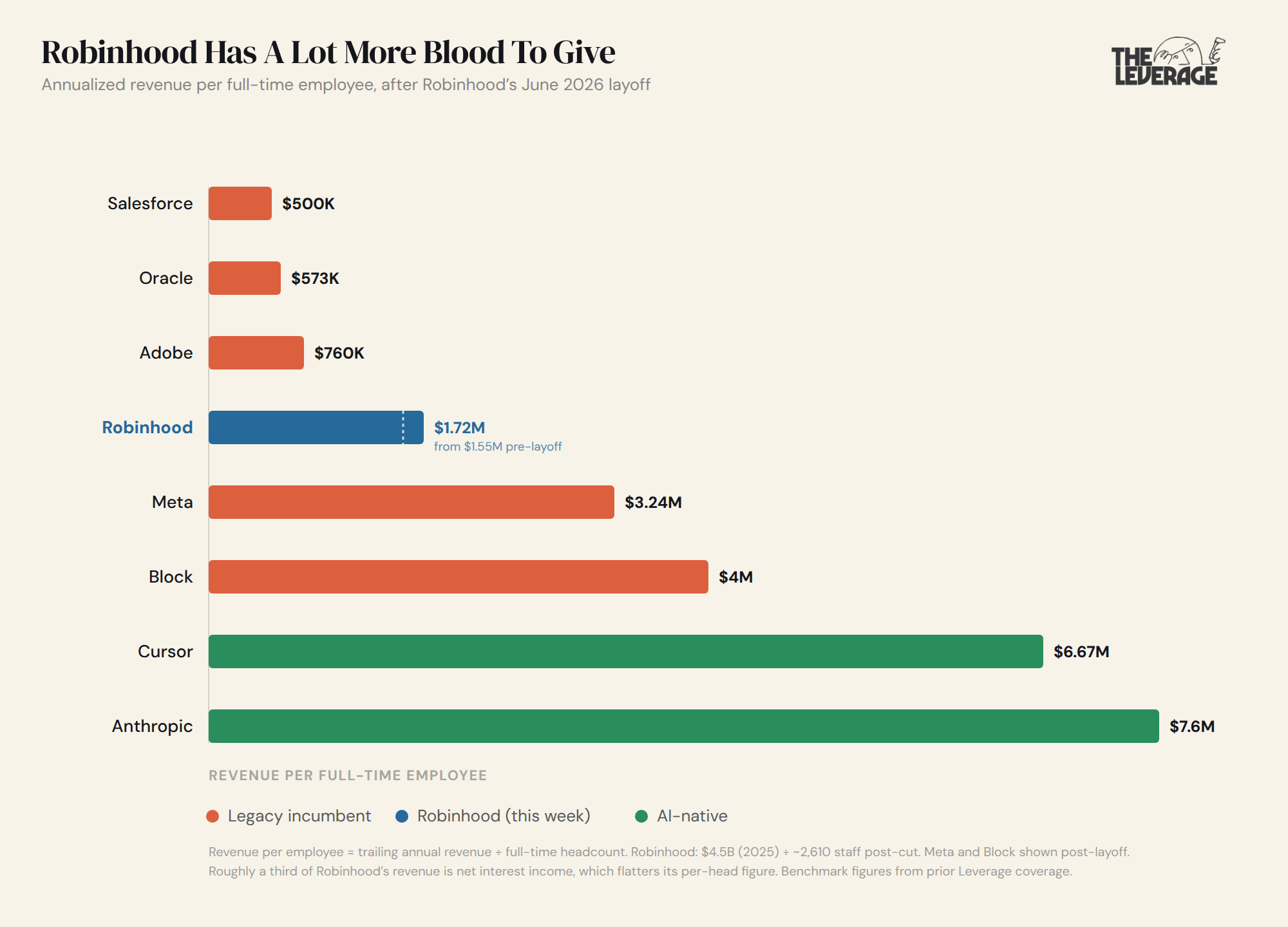

Robinhood is out for employee blood. On June 16, Robinhood cut roughly 290 people, about 10% of its staff. It did this nine days after telling the SEC that June trading volumes were at record levels across equities, options, and prediction markets, four months after closing the best year in its history. Despite that, the stock rose more than 2% on the news. In the announcement, Vlad Tenev told employees the company has “never been stronger.”

I am only sorta convinced by his argument. 2025 was a monster. The revenue was $4.5 billion, up 52%, with a net income of $1.9 billion, and a stock that rallied 220% on the back of prediction markets. This is not 2022, when Robinhood was losing $295 million a quarter and Tenev cut 23% of the company.

Once again, we are left to confront the reality that companies are just expected to run leaner now. Robinhood’s $4.5 billion across 2,900 people is about $1.55 million in revenue per employee. These cuts will pull it to $1.72 million. Here is where that lands the trading app relative to other tech firms this year:

That gap is at least part of the reason Tenev is cutting.

The other is that the golden goose has a case of “sell all my crypto blues.” Crypto was 2025’s rocket fuel, but that rocket is running on fumes, earning $268 million in Q3 to $134 million in Q1 2026, down nearly 50% in two quarters. While total Q1 revenue grew 15% to $1.07 billion, it was because options, net interest, Gold, and prediction markets covered the firm’s butt. But the highest-margin, most-volatile line on the income statement lost half its value in six months, and 290 salaries is the offset.

Three things are true here. One, this is margin defense dressed as culture. It is the revenue-per-employee reset I keep writing about, because the market now pays for efficiency. He is not alone. Coinbase cut 700 people, 14% of staff, a month earlier, blaming crypto headwinds and the AI era. The crypto houses are all trimming as the 2025 sugar high wears off, each reaching for a different word for the same move.

The takeaway is the one I have made since Block. The revenue-per-employee bar is being reset in real time, and the companies resetting it are no longer the ones in trouble. Robinhood laid off 10% of its workforce four months after its best year ever, and Wall Street said thank you by raising its stock price. When healthy companies cut to hit efficiency numbers, I think there are a lot more jobs left to go.

BIG ACQUISITION

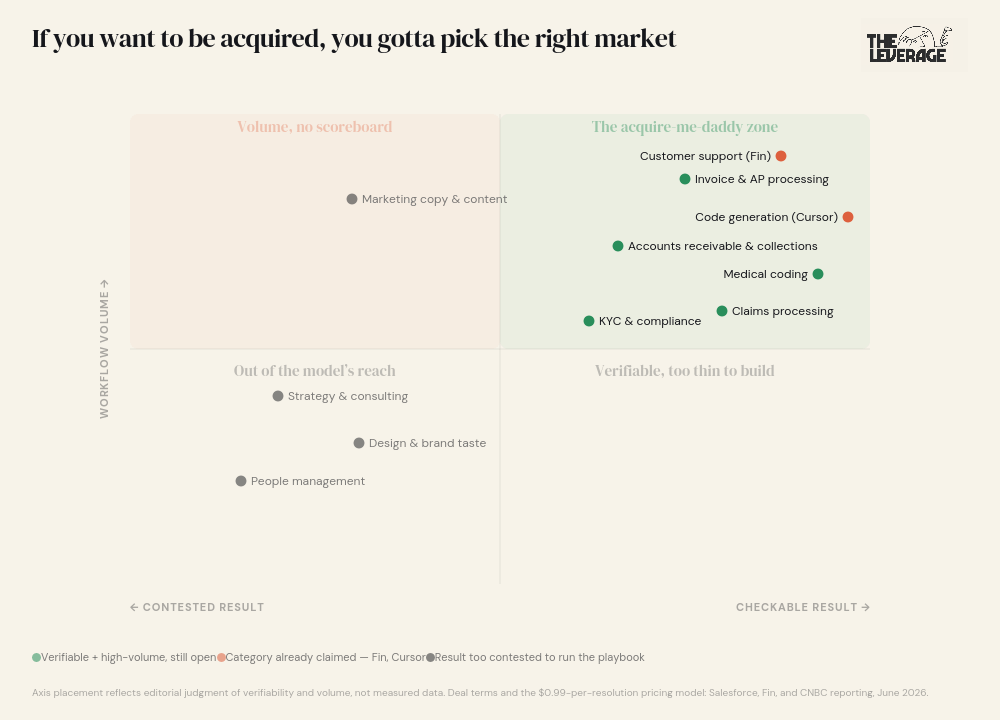

The “Acquire Me, Daddy” Playbook. Within 24 hours last week, 2 companies got bought for running the same playbook. On June 15, Salesforce agreed to buy Fin (formerly Intercom) for ~$3.6 billion. On June 16, SpaceX confirmed it would acquire Cursor parent Anysphere for $60 billion in stock, 4 days after the rocket company’s record Nasdaq debut.

These two acquisitions show how great AI-native startups can be built. The playbook has 4 steps:

1. Pick a workflow with verifiable results. Fin chose customer support, where a resolution is a discrete, countable event. The firm closes 76% of support volume with no human in the loop. Cursor chose code, where the output either compiles and passes tests or it doesn’t. Both startups worked in domains where “did the AI actually do what it is supposed to” has a real answer.

2. Go AI-native inside the product, not in a chat window next to it. Their product suites were not old school SaaS workflows with models tacked on. They fundamentally reimagined what work could be done with LLMs and built accordingly.

3. Tie the price to the result. Fin helped pioneer outcome-based pricing by charging $0.99 per resolution. Regular readers know I’ve argued that outcome pricing erodes your margins and hands your upside to the customer. My two carveouts were in customer support and coding. Vindicated once again!

4. (Most important) Build a custom model to own the margin. Fin started on GPT-4, leaned on Claude, then post-trained its own model, Apex, purpose-built for support and claiming better resolution than OpenAI and Anthropic. Cursor had been training its own models on xAI chips, and cutting frontier-model dependence is the explicit prize for SpaceX. The custom model converts you from a wrapper to an asset.

A great market for AI workflows is high volume work with checkable results.

The more I think about this, the more I’m convinced there’s an enormous number of AI native firms that could be running these playbooks right now. Reach out if you feel you are building one of them! Speaking of AI native…

BIG RESEARCH

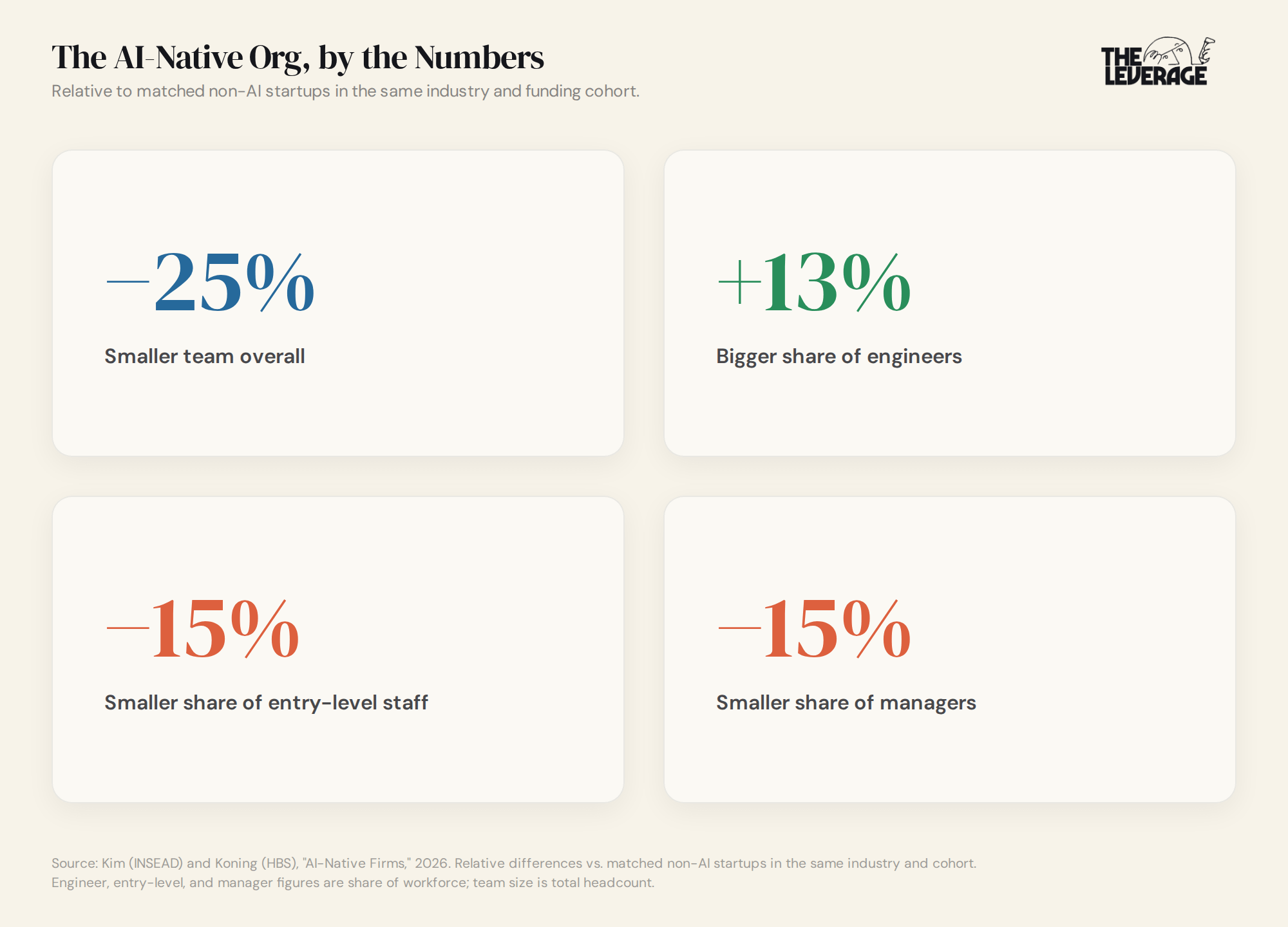

What is an AI native firm again? For the last 6 months, I’ve been arguing that AI-native firms are a fundamentally different type of startup that requires all new playbooks. Here is some more evidence in favor of that argument. Researchers at INSEAD and HBS classified the AI-native status of every Y Combinator company from winter 2020 through fall 2024, added the US venture-backed startups that raised a first round between 2020 and 2024, and matched each one to workforce data on size, function, and seniority. (paper here)

The results are, uh, crazy.

This is the cleanest empirical case yet for the thing this newsletter has been arguing for. While staffing differently and more leanly, they do it at comparable valuations, which means more value per employee, a metric I will not shut up about.

The researchers found that most of the leanness comes from the product channel. AI-native firms embed the intelligence into what they sell, so the product does the knowledge work that headcount used to. The authors separate this from the process channel, where employees just layer AI tools onto existing workflows.

This is deeply exciting to me. We are entering a whole new world! I have some essays in the hopper that will help you make sense of it all.

Go and be kind this week,

Evan

Sponsorships

We are now accepting sponsors for the Q3 ‘26. If you are interested in reaching my audience of 35K+ founders, investors, and senior tech executives, send me an email at team@gettheleverage.com.

The shopping spree is the tell. When capital this concentrated starts buying instead of building, it signals the build-vs-buy math has flipped for AI assets. For everyone downstream, the real question is whether you're an acquisition target or a rounding error. Worth watching what gets bought, not just who's buying.