Data Centers are Gobbling up All the Capital

The Weekend Leverage, November 23rd

Nvidia smashed earnings and kept the music playing this week. VCs and AI investors breathed a collective sigh of relief—the company gave everyone permission to let the bubble inflate a little longer. Meanwhile, I’m drowning in news of oversized funding rounds. Anthropic raising $15 billion to fund training runs? Sure. Google holding meetings about how to “1000x AI infrastructure over the next 4-5 years?” Why not?

While all of this tastes sweeter than Grandma’s pumpkin pie to Nvidia stockholders, it’s slightly worrying. This story repeats every week: another massive raise, another ambitious infrastructure promise, another round of champagne. How much longer can this go on?

This edition we’ll get some signals on what can keep going (and what can’t):

The breakout AI consumer app that has infected YouTube

How transcription apps change the nature of computing

Elon Musk’s gigantic new capital raise

But first, this edition is brought to you by Wealthfront.

I keep my cash in Wealthfront because I’m too lazy to optimize it myself.

Look, I’m not trying to day-trade my emergency fund. I just want my money to actually work while it sits there.

Wealthfront’s Cash Account gives me 3.50% APY through program banks on money I’d otherwise leave rotting in a checking account. No monthly fees, no minimums, no thinking required. It’s FDIC insured up to $8 million through program banks, offers free instant withdrawal feature to eligible accounts, and I’ve been using it for years because it just... works.

I write about financial markets for a living and this is still the best place I’ve found for my cash before I’m ready to invest it in my other Wealthfront investing accounts.

Right now, you can get an extra 0.65% APY for three months on up to $150,000 when you open your first Cash Account. Go to wealthfront.com/theleverage to sign up today. Promo terms and conditions apply.

That’s a total 4.15% variable APY. Your savings account could never.

Evan Armstrong is a Wealthfront client and received compensation for the testimonial and promotion of the Wealthfront Cash Account. This compensation creates a conflict of interest. Experiences may vary among Cash Account clients, and results are not guaranteed.

MY RESEARCH

Doordash is out for blood. Because AI dramatically reduces the cost of code, founders suddenly have the budget/margin to be far more aggressive in their strategy. No company better exemplifies this than Doordash. They have simultaneously expanded internationally with a $3.9 billion acquisition of Deliveroo, launched a new autonomous delivery robot, and spent $1.2 billion buying a Vertical SaaS company. I had exclusive conversations with multiple members of their leadership team about the scope of their vision for this piece. Their idea is wildly audacious, but with the help of cheap AI code, they just might pull it off. Pay attention to this story, you’ll see every company go for this aggressive of a roadmap soon.

Google’s new image model is incredible. As someone who has been using various image models almost daily for the last few years, trust me when I say this is the one. It is finally good enough not just for some viral tweet saying “This will change everything” but actually has the ease of use/power to finally be integrated into the most sexy/most important thing in the world: B2B SaaS. And where the workflows go, the world follows. You should expect that every application that has even the barest hint of being boring (aka all of them) will try adding more visual intelligence to what they are doing. For paying subscribers, I list out prompts to try and how I expect applications to integrate this form of AI.

WHAT MATTERED THIS WEEK?

AI LABS

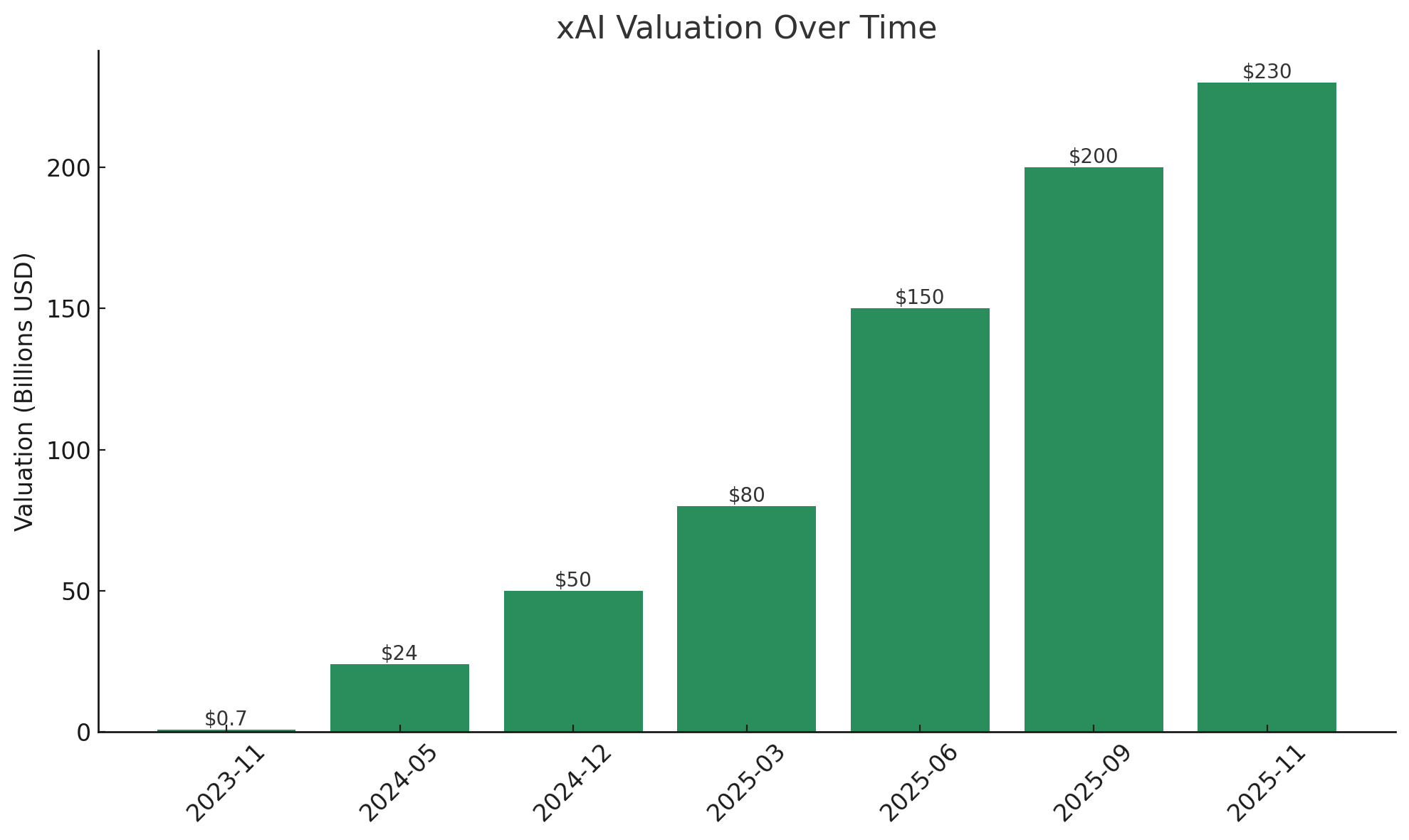

Elon Musk’s xAI valuation makes no sense. Look, I realize that Musk is God’s gift to wealth creation. It is hard to bet against him in the long-term. However, this is getting a little out of hand. News broke this week that his Temu brand OpenAI planned to “raise $15 billion in new equity at a $230 billion valuation.” This same startup was valued at $113 billion in March. March! One report from Reuters in June said that xAI’s expected revenue from 2025 was $1 billion while a report from Bloomberg a few days later pegged it a measly $500 million. Simultaneously, the firm is supposedly burning through $1 billion a month. Valuing something at 230x revenue that will burn through $10+ billion dollars in cash this year feels borderline criminal. That said, we have scant reporting on this company and I may be missing key facts. But I mean…look at this jump in valuation in just two years.

I know some of the investors in this company read me. If you want to talk about your thesis, my inbox is open! I’m genuinely curious to hear the bull case. Until I get new data, this is the company that most screams AI bubble to me. Price matters. Fiscal discipline matters. XAI appears to think that its founder’s track record frees it from both of those truths. They may find out it does not.

Can GPT-5 do science? A new paper released this week from OpenAI argues that it can. The paper’s core claim is pretty straightforward: GPT-5 can already make contributions to research but only inside workflows where humans are steering the ship and verifying every step. They’ve built a tool that reliably accelerates the middle of the scientific process without pretending to be the scientist.

My take is this sounds an awful lot like every other B2B SaaS product on the planet. It slips into the existing workflow, shaves off coordination overhead, and quietly increases throughput. GPT-5 isn’t some alien intelligence descending from the sky proclaiming it’s solved physics—it’s the world’s most overqualified research middleware, and that is both perfectly reasonable and exactly how general-purpose technologies have always entered the real economy. If anything, that it is so blasé is somewhat reassuring.

DEAL VIBES

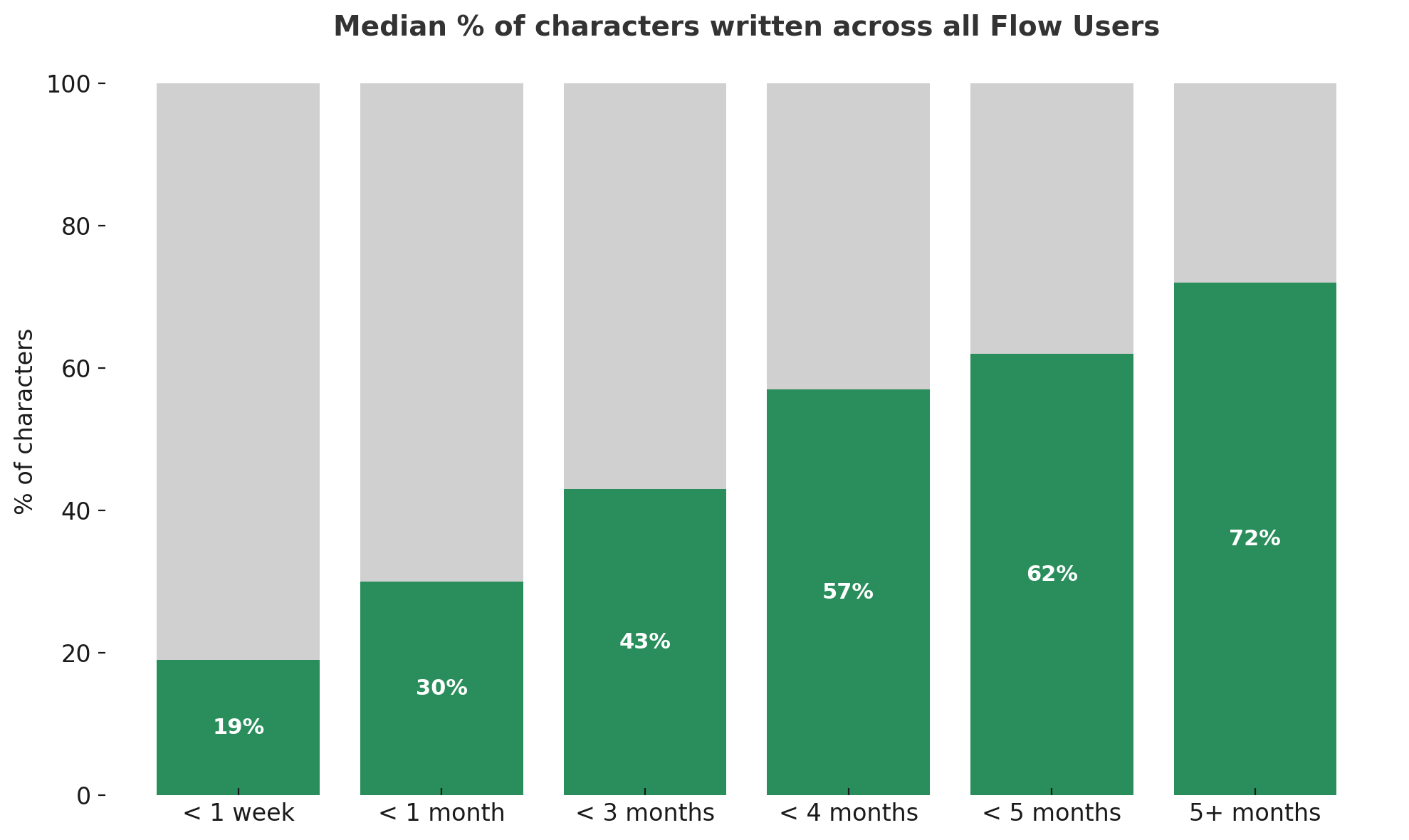

The computer will hear you now. Wispr is a dictation app that transcribes words you speak aloud into the app you have open. Essentially, this is an app that allows you to shoot the shit with your computer. The company raised a fresh $25 million in capital and boasts some impressive metrics like 100x user base year-over-year growth with 70% retention over 12 months. However, what actually caught my attention was how the users behaviors changed. Look at this:

Data provided by company here

For users who make it to the 5+ month mark, every three in four words is spoken versus typed. This is a fundamental evolution in how we interact with our devices. I’ve used the app for months and have found that the text I dictate is infinitely more casual, and also infinitely less thoughtful. Human beings speak about 150 words a minute on average, while the typical person can only type 50 words per minute. Personally, I don’t use it to write the newsletter—it’s for email and casual communication needs.

Since LLMs emerged, transcription tools have focused on capturing what I call “ambient data”—sales calls, meetings, recorded conversations. Those transcripts are then fed into an LLM to divvy up action items. Now with Wispr we are starting to see specialized applications that use transcription technology.

Which means the future may be less about tapping at glass and more about talking into the air—computers not as tools we operate, but as companions that catch whatever words happen to fall out of us. And that’s the real story here: once speaking becomes the primary interface, the entire texture of digital communication shifts. Wispr enables a new primitive for knowledge work, and I’m still unsure of how long-term that shifts our interactions with work. If the medium is the message, what message does a spoken-word-computer medium have?

AI music is the new breakout consumer app. While ChatGPT has soaked up most of the attention, Suno is a true consumer breakout hit with over $200 million in revenue. They raised $250 million at a $2.45 billion valuation on the back of that growth. The company sells membership tiers and “top-off” credits. For all consumption based experiences like Suno, your money is either made in users not fully utilizing their accounts (bad) or in people never having enough credits (bad, but in a different way). The first category is in the top of funnel business, while the second is about finding and keeping whales. Suno is in the latter category. They make money when people get obsessed with their product and don’t want to stop generating songs. Which…feels great? Generating music and jamming out seems like a relatively healthy way to spend time on a computer. Plus, I think the team comes at it from the right place. I hung out with Mikey, the CEO and co-founder in their Cambridge, Massachusetts office late last year and was impressed with his love of music. One interesting wrinkle: they allow users to retain commercial rights to the music they generate—more on why this is important in a second.

As I warned you, the robots are coming. Physical Intelligence, a company that makes AI software for robots, raised $600 million at a $5.6 billion valuation. I covered this company fairly extensively two weeks ago, but essentially they are trying to make a mega brain that can be stuck into any robot. This is an ambitious vision, but the company is staffed with many of the most important researchers in the industry, so they have a shot. The team has lots of hype in the valley with multiple investors telling me that Physical Intelligence, “reminded me of early OpenAI.” I’ll have more on what makes their technology unique in the coming days for paying subscribers.

TASTEMAKER

Oink, oink. Slop, slop. I’ve been jamming out to city pop for the last 6 months. The genre comes from Japan in the 1970s and 80s, and is a mix of funk, disco, and soft rock that feels “metropolitan” for lack of a better descriptor. To start learning about the genre, I listened to vinyl mixes from DJs. Then I got algorithmically recommended this video on YouTube called “K Y O T O 1 9 8 0 - 日本のシティポップ 80’S JAPANESE CITY POP.” As the hour mix went on, my ear caught a few things that sounded just a little…off. Still, people in the comments section were really feeling something.

I paused my writing to listen to the mix a little more closely. To my horror, I realized that the entire thing was just AI music. I’d been mindlessly consuming slop for about 30 minutes. It’s partially why the Suno deal this week caught my eye. Whoever is the owner of that Youtube channel realized there was an arbitrage between the cost of the tokens to generate these songs and the Youtube payout. Suno’s policy of having users owning commercial rights led to me wasting my time on this mix. On the other hand, I don’t speak Japanese and didn’t live during the 80s. Is there any real difference, to an uneducated consumer like me, between the authentic and the AI?

It’s why I consider the central problem of AI content not its existence, but because of consumer ignorance. Are there people creating products that teach the general populace how to develop taste?

Have a great week,

Evan

Sponsorships

We are now accepting sponsors for the Q1 ‘26. If you are interested in reaching my audience of 35K+ founders, investors, and senior tech executives, send me an email at team@gettheleverage.com.

If you are eligible for the overall boosted rate of 4.15% offered in connection with this promo, your boosted rate is also subject to change if the base rate decreases during the three-month promotional period.

The Cash Account, which is not a deposit account, is offered by Wealthfront Brokerage LLC (”Wealthfront Brokerage”), Member FINRA/SIPC. Wealthfront Brokerage is not a bank. The Annual Percentage Yield (”APY”) on cash deposits as of November 7, 2025, is representative, requires no minimum, and may change at any time. The APY reflects the weighted average of deposit balances at participating Program Banks, which are not allocated equally. Funds in the Cash Account are swept to Program Banks where they earn a variable APY and are eligible for FDIC insurance. Conditions apply. For a list of Program Banks, see: www.wealthfront.com/programbanks. FDIC pass-through insurance, which protects against the failure of Program Banks, not Wealthfront, is not provided until the funds arrive at the Program Banks. While funds are at Wealthfront Brokerage, and while they are transitioning to and/or from Wealthfront Brokerage to the Program Banks, the funds are eligible for SIPC protection up to the $250,000 limit for cash. FDIC insurance is limited to $250,000 per customer, per bank, regardless of whether those deposits are placed through Wealthfront Brokerage. You are responsible for monitoring your total deposits at each Program Bank to stay within FDIC limits. Wealthfront works with multiple Program Banks to make available up to $8 million ($16 million for joint accounts) of pass-through FDIC coverage for your cash deposits. For more info on FDIC insurance coverage, visit www.FDIC.gov.

Instant and same-day withdrawals use the Real-Time Payments (RTP) network or FedNow service. Transfers may be limited by your receiving institution, daily caps, or participating entities. New Cash Account deposits have a 2–4 day hold before transfer. Wealthfront does not charge fees for these services, but receiving institutions may impose an RTP or FedNow Fee. Processing times may vary.

Didn't expect this take, but you nail the bubble worries. Still, gotta have that compute power, no?